A 35-Year Career, a ₹6,000 Pension — Why This Needed Raising

A colleague of mine retired after 35 years of service. Thirty five years of EPF deductions, employer contributions, all of it. His EPS pension came out to six thousand rupees a month.

Six thousand. In today’s market, that is not an amount that can even keep a person going, forget anything beyond survival. As a PSU employee, I cannot look at that number and tell myself I can rely on EPS alone for my own retirement.

That number is what pushed a few of us in our employee union to take this up with management.

EPS-Only vs NPS: What’s Actually Missing

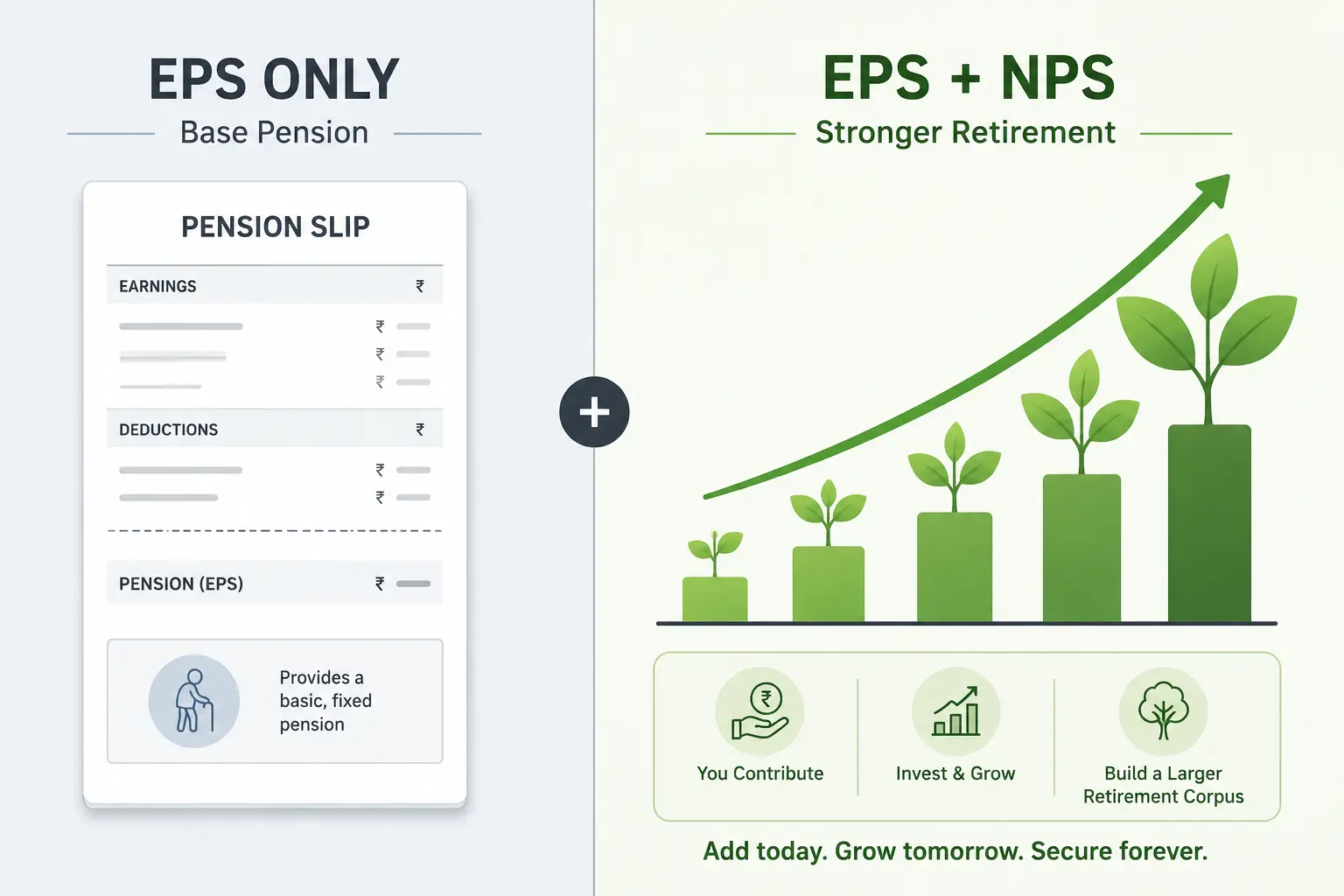

That six thousand rupee figure was not some calculation error. EPS pension is worked out using a fixed formula: pensionable salary multiplied by years of service, divided by 70. The catch is that pensionable salary is capped at ₹15,000 a month for EPS purposes, no matter what your actual basic salary is.

Run the numbers and the ceiling becomes obvious. Even with the maximum 35 years of service counted, the highest EPS pension anyone can get under this formula is about ₹7,500 a month. My colleague’s actual pensionable salary worked out lower than the ₹15,000 cap, which is how he ended up at six thousand.

This is what EPS-only employees are missing: a way to make your retirement income grow with your actual salary instead of getting stuck behind a ₹15,000 ceiling. NPS does not replace EPS. It sits alongside it as a separate, market-linked account where contributions, yours and your employer’s, are based on your real basic pay and Dearness Allowance, with no ceiling like the EPS one.

Over 25 to 35 years, that difference compounds into a separate pension pot that has nothing to do with the ₹15,000 cap. That is the entire gap our PSU does not have.

It’s Not Just Me — Why New Joiners Keep Asking the Same Question

When I joined this PSU as a new employee, one of my first questions was why there was no NPS option. I had heard about it elsewhere and wanted to know if it applied to us. I did not get a clear answer back then either.

Years later, a fresh graduate joined our team. He had done his homework and knew exactly what NPS was, how it worked, and what it offered. His question to me was almost identical to the one I had asked when I started: why does our PSU not have this?

That gap between two new joiners, years apart, asking the same question tells you something. This is not a one-off complaint from someone confused about retirement planning. It is a recurring question every fresh batch eventually runs into, once they actually look into what other organisations offer their employees.

What We Learned From a Friend at a Nearby Maharatna PSU

Around the same time, I got talking to a friend who works at a nearby Maharatna PSU. I asked him a simple question: what do you actually get from your organisation for retirement? His answer surprised me.

His PSU runs its own provident fund trust instead of being linked to EPFO. On top of that, they have their own NPS structure for employees, following IDA pay structure and DPE guidelines, similar to how central government bodies are set up. According to him, NPS was simply built into how the organisation already worked.

I want to be upfront here. This is based on what a friend shared in conversation, not an official circular I have personally seen. Every PSU sets its own retirement benefit structure depending on its trust deed and DPE category, so what one Maharatna offers is not a guarantee for another.

What it told me, though, was that NPS in a PSU is not some impossible ask. Somewhere close by, a comparable organisation had already worked it into their structure. That made our own management’s response harder to simply accept at face value.

What We Actually Asked Management For — and Why It’s Not Free

When we sat down with management, we were specific about what we wanted. We did not ask for permission to open individual NPS accounts on our own, because employees can already do that without anyone’s approval. We asked the organisation to adopt the Corporate NPS model and contribute to it on our behalf.

That distinction matters because it changes who pays. Under the Corporate NPS model, the employer contributes up to 14 percent of an employee’s basic pay and Dearness Allowance into the NPS account, on top of whatever the employee puts in themselves. For one employee that sounds manageable. Multiply it across an entire PSU workforce, every single month, and it becomes a real recurring cost on the organisation’s books.

This is also the part that actually moves the needle on retirement income. An employee opening their own NPS account gets the market-linked growth, but the size of that account depends entirely on what they can afford to put in. Get the employer to contribute 14 percent as well, and the corpus builds faster, funded partly by the organisation, not just out of an already stretched salary.

We knew this would cost the PSU real money. That was the point. We were not asking for a symbolic gesture. We were asking management to put their share into something that would actually change what people like my colleague retire with.

“Budget Constraints” — Where the Ask Stands Today

Management’s response came down to one thing: budget constraints. They were not dismissive about it, and to be fair, it is not an unreasonable answer. Contributing up to 14 percent of basic pay and Dearness Allowance into NPS for every employee, every month, adds up to a real number on the PSU’s expense sheet, not a one-time cost.

That is exactly where things stand right now. The ask has not moved forward. There has been no second round and no formal rejection either, just a budget constraint that nobody on our side can argue away with facts, because it genuinely is a cost the organisation has to absorb.

I am not writing this section to make management look unreasonable. I am writing it because “budget constraints” is a real, valid reason, and PSU employees deserve to know that this is genuinely where these conversations get stuck. Not because anyone is being difficult, but because someone has to actually pay for it.

What This Means for You If Your PSU Has No NPS Either

If your PSU also has no NPS, the first thing to actually check is what your provident fund deductions say. Look at your payslip and ask your HR or PF section directly whether your organisation runs through EPFO or its own exempted trust, and whether NPS exists in any form. Do not assume it works the same everywhere.

If there genuinely is no employer-backed NPS, you are not locked out of it. You can open an NPS Tier 1 account on your own through any bank or the eNPS portal, with no employer involvement needed. You will not get the 14 percent employer contribution we asked management for, but your own contributions still qualify for the extra fifty thousand rupee deduction under Section 80CCD(1B), if you are on the old tax regime.

If you want your organisation to actually contribute, the ask needs to be specific, the way ours was. Take the Corporate NPS model by name to your employee union or association, not a vague request for “better retirement benefits.” Vague asks get vague answers. Specific asks at least get a specific reason, even if that reason is budget constraints.

What I will not tell you is that this gets fixed quickly. Ours has not. If your PSU is EPS-only like mine, start your own NPS account this year regardless of what management decides, because your retirement math does not wait for an organisation’s budget cycle to clear.