Why Your Salary Slip Is the Most Important Document You’re Ignoring

Every month, without fail, your salary slip lands in your inbox or on your ESS portal. And every month, most PSU employees do one of two things with it — check the net pay figure at the bottom, or download it and forget it until the bank asks for it during a loan application.

That’s it. That’s the entire relationship most government employees have with the most important financial document they receive every single month.

Here’s what they’re missing.

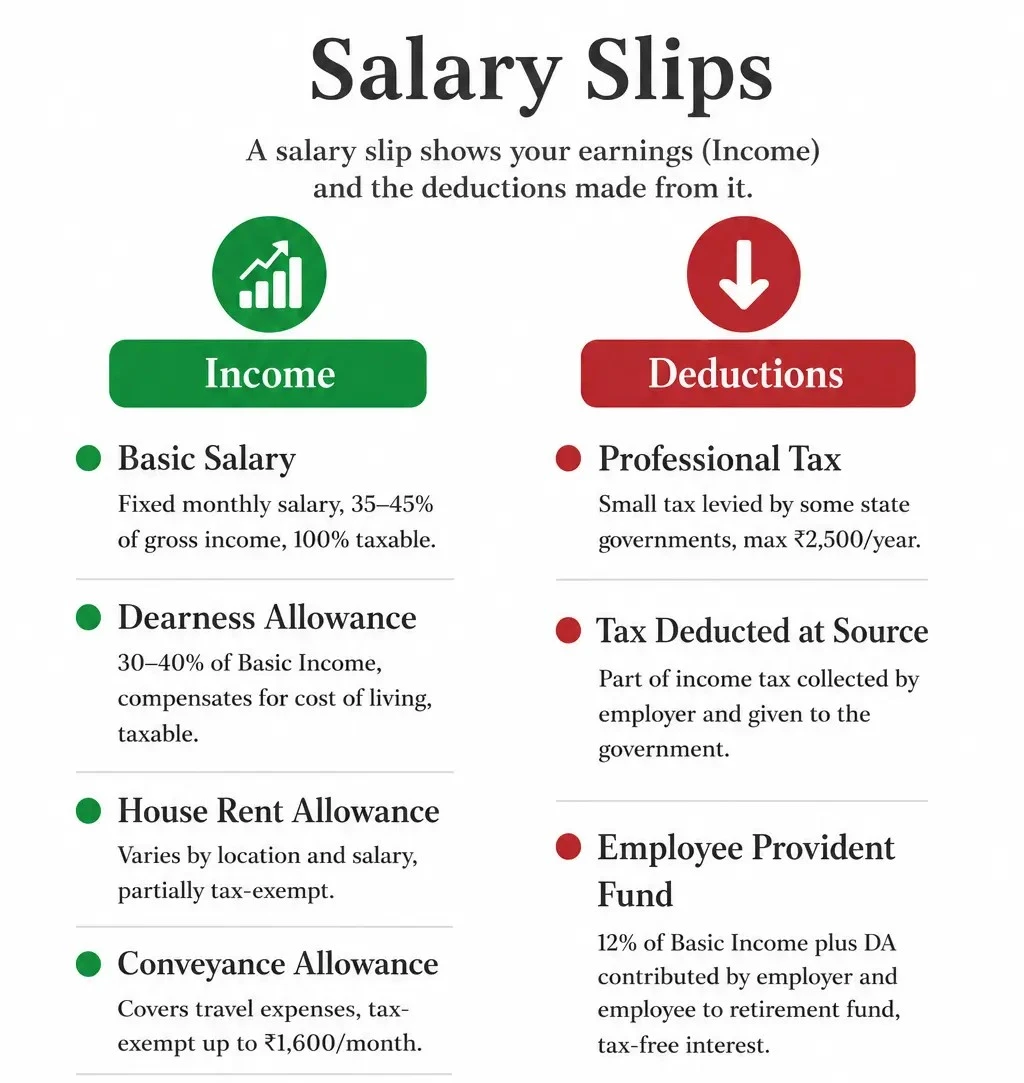

Your salary slip is not just a payment receipt. It is a calculation sheet — a detailed breakdown of exactly how your employer arrived at that final number in your bank account. Every line has a meaning. Every deduction has a logic.

And that logic, when you understand it, tells you things that matter: whether your tax regime is correctly applied, whether every allowance you’re entitled to is actually being paid, whether a deduction is correct or has crept in by error.

And errors do happen. The system is not always accurate. A wrong DA calculation, a Children Education Allowance that stopped without notice, a deduction that continued after a loan was closed — these things happen in PSU payroll departments. The employee who reads their slip catches it. The employee who only checks the net pay figure funds someone else’s mistake for months without knowing.

Beyond catching errors, your salary slip tells you something more valuable: which components are working for you and which are quietly draining you. Your earners and your deduction suckers. Once you know the difference, you start making smarter decisions — about loans, about tax planning, about how much of your gross is actually yours to plan with.

This article is going to show you exactly how to read it. Line by line. No jargon.

The Header Section — Your Basic Details

Before you get to any numbers, your salary slip opens with a header section that most employees scan past without reading. Don’t.

A typical PSU salary slip is divided into three broad parts. The first is the header — basic details about your organisation and you as an employee. This includes your name, employee ID, designation, grade, department, location, date of joining, bank account number, UAN for PF, PAN, and your chosen tax regime.

The second part is the earnings and deductions table — the heart of the slip, where every rupee you earn and every rupee that gets cut is listed line by line. The third part is the perks and taxation summary — a Form 16 style grid showing your projected annual income, perks value, and estimated tax liability for the year.

Every organisation structures these three parts slightly differently. The components may vary, the layout may look different, and some allowances will exist in one PSU that don’t exist in another. But this three-part structure — details, earnings and deductions, taxation — is the common skeleton across most government and PSU payslips in India.

Now, for a new joiner receiving their first salary slip: the single most important thing to check is your salary structure. Not the net pay. The structure. Verify that your scale pay and grade pay match your appointment letter. Verify that your designation and grade are correctly recorded. Verify that your tax regime (read more on this) reflects what you actually chose on the ESS portal. These details sitting wrong in the system from Day 1 can silently affect your TDS, your loan eligibility, and your increments for months before anyone catches it.

Read the header. It takes two minutes. Do it every April when your increment kicks in.

Scale Pay — The Number That Grows With You

The first earning component on your salary slip is your Scale Pay — and it’s the most important number to understand because everything else is either added to it or calculated as a percentage of it.

Your designation determines which pay scale you fall under. Within that scale, there is a starting pay and a ceiling pay. Every year on your increment date, your scale pay grows by 3% automatically. You don’t apply for it, you don’t negotiate it — it happens by rule. Show up, do your job, and your scale pay quietly rises every April.

When you get promoted to a higher designation, your scale pay jumps to the starting point of the new, higher scale. Two growth engines working together — the steady 3% annual climb within your current scale, and the bigger jump when a promotion kicks you into the next one.

The second component sitting right below it is your Grade Pay — a fixed amount attached specifically to your designation level. Unlike scale pay, grade pay doesn’t grow annually. It only changes when your designation changes through promotion.

Put these two together — Scale Pay plus Grade Pay — and you get your Basic Pay. That single combined number is the foundation of your entire salary structure. Your Dearness Allowance, your PF contribution, your Transmission Allowance — all of them are calculated as a percentage of this Basic Pay. Which means every time your scale pay grows by 3% on increment day, a ripple effect moves through your entire salary.

Every DA-linked component rises. Every PF contribution rises. The increment is never just the increment.

One noticeable thing here is that pay structures vary between central PSUs, state PSUs, and government departments. So, be smart and check your salary slip carefully.

Grade Pay — Your Designation’s Rank in Rupees

Grade Pay is the second component of your Basic Pay, sitting right alongside your Scale Pay on the salary slip. Together they form the foundation of everything else.

Think of Grade Pay as your designation’s rank expressed in rupees. Every designation level in your organisation has a fixed Grade Pay attached to it. A junior level employee has a lower Grade Pay. A senior officer has a higher one. It is the salary structure’s way of acknowledging not just what you earn today, but where you stand in the organisational hierarchy.

Unlike Scale Pay which grows 3% every year automatically, Grade Pay is completely static until your designation changes. It doesn’t move with increments, it doesn’t adjust with inflation, and no amount of good performance moves it. The only thing that changes your Grade Pay is a promotion to a higher designation.

It is also important to understand that Grade Pay is not universal. Central PSU employees, state PSU employees, and central or state government employees all follow different pay structures governed by their respective pay matrices and pay revision committees.

A Grade Pay of ₹4,200 in one structure does not mean the same thing as ₹4,200 in another. What matters is the pay matrix your specific organisation follows — that is the rulebook for your Grade Pay, your Scale Pay, and every increment and promotion that follows.

So when a colleague from a different PSU or a government department quotes their Grade Pay to you, don’t compare numbers directly. Compare designations and responsibilities instead. The numbers mean different things in different structures.

Dearness Allowance — The Silent Raise You Get Twice a Year

Dearness Allowance is the component on your salary slip that most employees understand the least and benefit from the most.

DA is calculated as a percentage of your Basic Pay and is revised twice every year — in January and July — by the government. Each revision is linked to the Consumer Price Index, which means DA moves with inflation. When the cost of living rises, DA rises with it. It is the government’s built-in mechanism to ensure your real purchasing power doesn’t quietly erode while prices around you climb.

Currently DA sits at 60% of Basic Pay — effective January 2026 after a 2% hike. For context, on my Basic Pay of ₹37,720 (Scale Pay plus Grade Pay), that 2% hike translates to roughly ₹600 to ₹700 extra in my monthly take home. Not a dramatic number in isolation.

But I recently enrolled my child in school, and that ₹600 to ₹700 every month goes directly toward managing that new education expense. The timing was fortunate. The point is real — DA hikes are not just percentages on paper. They are actual rupees that show up when life gets more expensive.

Here is the part most PSU employees don’t fully appreciate: DA doesn’t just add to your take home. Because DA is linked to your Basic Pay, every time your Basic Pay grows through an annual increment, your DA amount grows too — even without a new DA revision.

A 3% increment in April doesn’t just raise your Scale Pay. It raises your DA, your PF contribution, your Transmission Allowance — everything that is calculated as a percentage of Basic Pay moves together.

This compounding effect is the silent wealth-building engine of a PSU career. It works whether you’re paying attention or not. But the employees who understand it plan around it — and that planning makes a real difference over a 30-year career.

Transmission Allowance — Your Daily Commute, Paid

Transmission Allowance — or Conveyance Allowance as some organisations call it — is one of those components that quietly separates PSU employment from most private sector jobs and almost all state government positions.

The concept is simple: you travel to the office every day, you spend money doing it, and your employer compensates you for that expense. That’s the allowance. Your daily commute, partially paid.

What most employees don’t realise is that this allowance is not universal. Most central and state government employees don’t get it at all, or receive a much smaller fixed amount. It is largely a PSU benefit — and not every PSU structures it the same way.

In our organisation, the Transmission Allowance has an interesting history. For years it was slab based — fixed amounts tied to your designation bracket, regardless of your actual Basic Pay. It was functional but limited, and for many employees it hadn’t kept pace with rising fuel costs and commute expenses.

That changed after the 2024 negotiations between the Trade Union and Management. The Union pushed for the allowance to be linked directly to Basic Pay instead of a fixed slab — and won. The result was significant.

Because Basic Pay grows every year through increments and DA revisions, linking Transmission Allowance to Basic Pay means it now grows automatically with your salary. Every increment day — your Transmission Allowance moves with it.

It is a small example of why Trade Union participation matters in PSU employment. One negotiation in 2024 means every employee in the organisation gets a higher TA every single year going forward, without asking for it again.

Children Education Allowance — Only If You Qualify

Children Education Allowance (CEA) is one of the most underutilised benefits in PSU employment. Eligible employees either don’t claim it on time, don’t know the correct slab, or simply forget to update it when their child moves to a higher class. All three are expensive mistakes.

The eligibility is straightforward but has clear boundaries. You must have a child currently studying — in school, college, or a professional course. If you don’t have children, this allowance doesn’t apply. If your child has completed education and is earning independently, you lose eligibility. The allowance exists specifically for the active years of your child’s education, and not a day beyond.

In my organisation, the allowance is structured in five slabs based on the level of education:

Class 0 to 5: ₹2,200 per month, Class 6 to 10: ₹2,900 per month, Class 11 to graduation: ₹3,600 per month, Post graduation or Masters: ₹4,300 per month Professional post graduation: ₹5,700 per month.

Every time your child moves to a higher education level, your CEA slab jumps up automatically — provided you inform your HR department with the correct documents. That last part is where most employees lose money. The jump doesn’t happen on its own. You have to initiate it with your employer.

Two things to do right now if you have a school or college going child: first, verify that CEA is actually appearing on your salary slip. Second, confirm that the slab matches your child’s current education level. If either is wrong, raise it with HR immediately. Every month you delay is money left on the table.

Wash/Kit Allowance — Small Amount, Real Purpose

Wash and Kit Allowance is the smallest component on your salary slip and also the simplest to understand.

Not every PSU provides this allowance — it depends entirely on your organisation’s pay structure and agreements. In my organisation, it exists for a practical reason: maintaining the dress code. Certain departments like security have their own uniforms.

Civil office staff receive an annual or bi-annual dress allowance for formal office wear. This monthly Wash and Kit Allowance is the organisation’s way of helping employees keep those uniforms and formal clothes clean, presentable, and in good condition. Office decorum maintained, expense partially covered.

The amount is small — don’t expect it to cover your dry cleaning bill. But it arrives every month without any condition, any document, or any application. It is one of those quiet, automatic benefits that adds up over a full career without ever demanding your attention.

If your slip doesn’t show this allowance and your colleagues’ slips do, raise it with HR. Small amounts ignored consistently become significant amounts lost permanently.

The Deduction Side — Where Your Money Goes Before You See It

Before a single rupee reaches your bank account, a set of deductions has already left your salary automatically. No approval needed from you, no reminder sent to you. It simply goes.

The largest and most important deduction is your PF contribution — 12% of Basic Pay every month, going straight into your EPFO account. On my salary that’s ₹7,152 per month, or ₹85,824 silently building every year. But here’s what most employees don’t realise: your employer contributes another 12% on top of that — matching your contribution entirely.

However, the employer’s 12% is split into two parts. 3.67% goes directly into your EPF account as additional savings. The remaining 8.33% goes into the Employee Pension Scheme (EPS) — a separate pension pot that determines your monthly pension after retirement. The EPS contribution is capped at ₹1,250 per month regardless of your actual salary level, because it is calculated on a statutory wage ceiling of ₹15,000.

So every month, your PF account is actually receiving contributions from two sources — yours and your employer’s — while a portion quietly builds your future pension in EPS. The current EPF interest rate for FY 2025-26 is 8.25% per annum, compounded annually.

Most employees never check their EPFO balance. They should. It is the single largest forced savings instrument in your entire financial life and it compounds quietly over a 30 year career into a number that will matter enormously at retirement.

Then come the accommodation related deductions if you live in company provided quarters — rent, electricity, water, PNG or gas charges. These vary depending on the quarter type and your grade level. Small individually, but combined they add up to a meaningful monthly outgo.

Club memberships, trade union memberships, and welfare fund contributions follow — small fixed amounts that most employees pay without fully understanding what they’re enrolled in. Know what you’re a member of. Know what benefit it provides. Don’t just let it leave your salary on autopilot for decades.

Then there is the GSS — Group Superannuation Scheme. This is the deduction that took me the longest to understand, and honestly, I’m still not entirely satisfied with my understanding of it. It is our organisation’s dedicated retirement scheme, tied up with LIC of India. It is not NPS, not UPS, not a standard pension product you can easily look up.

Currently 1% of Basic Pay is deducted from the employee and matched by 1% from the employer — 2% total going toward this scheme every month. The troubling reality: senior employees who retired from top level pay grades are receiving only ₹8,000 to ₹12,000 per month from this scheme.

For a career spanning 30 plus years, that monthly pension amount raises serious questions about the scheme’s structure and returns. As part of the trade union, we are actively pushing to increase contributions to 5% from both sides — 10% total — to make the retirement corpus more meaningful.

Finally come your loan EMIs — Home Building Loan, vehicle loan, any salary advance taken from the organisation. These appear clearly on your slip with the outstanding balance alongside the monthly deduction. Check the outstanding balance every month. Know exactly when each loan closes. The month a loan closes is the month your cash flow breathes again.

The Form 16 Summary Grid at the Bottom

At the bottom of your salary slip sits a small grid that most PSU employees ignore for the first several years of their career. I did too. Until the month I noticed tax being deducted from my salary and couldn’t understand why.

My gross salary wasn’t crossing the taxable threshold — at least not the number I was mentally calculating. So I raised it with my accounts department. That’s when I learned something that nobody had explained to me during joining: perks are taxable income.

Company provided accommodation has a monetary value assigned to it by the Income Tax rules. A subsidised Home Building Loan — where you pay interest below market rate — has a perquisite value calculated on the difference between what you pay and what the market charges.

These perks get added to your gross salary for tax calculation purposes, even though you never see that money in your bank account. The quarter you live in, the cheap loan you’re repaying — both push your effective gross salary higher than your slip’s earnings total suggests. High enough, in my case, to cross the taxable threshold.

This is what the Form 16 summary grid at the bottom of your slip is showing you every single month. Your projected annual gross salary including perks, your estimated tax liability based on your chosen regime, and the standard deduction already applied.

Most employees check this grid once a year — in March when HR sends the investment declaration reminder, or during ITR filing in July. By then it’s too late to course correct. Check it every month. Specifically look at two things: the perks value being added to your gross, and whether the resulting tax liability matches what is actually being deducted from your salary.

A mismatch caught in June is a problem solved easily. The same mismatch caught in February means 10 months of wrong TDS already deducted and a refund process waiting for you.

4 thoughts on “How to Read Your PSU Salary Slip — Every Component Explained Simply”