Your Salary Looks Bigger This Month — But It’s Not What You Think

You open your salary slip this month and something feels different. The number at the bottom is higher than usual. No promotion. No increment. Just a fatter figure sitting there quietly.

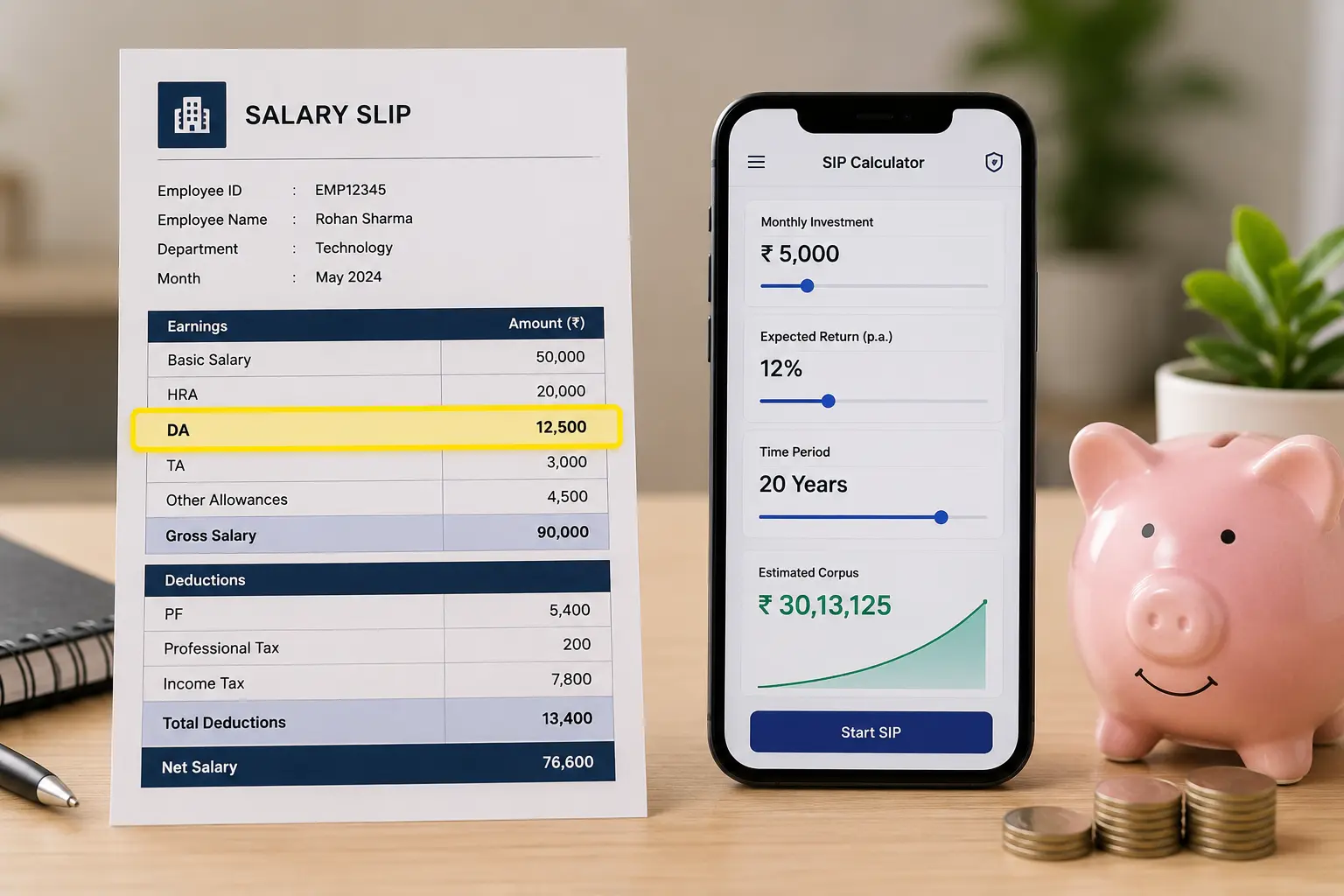

That’s your DA arrears. The Assam state government recently hiked DA from 58% to 60% of basic pay. For state PSU employees whose DA follows the state rate, this means 3 to 4 months of arrears landed in one salary — mixed in silently, no separate alert, no special credit.

Most employees do exactly two things at this point. First, they check if the amount looks right. Second, they start thinking about expenses — EMIs, a pending bill, something the family has been asking for. The money feels like a bonus. So it gets treated like one.

Here is the problem. This is not a bonus. It is a structural pay increase that will repeat every 6 months. And if you do not decide what to do with it before it hits your account, your expenses will decide for you.

What Is DA and Why Does It Get Hiked Every 6 Months?

Private sector employees get yearly appraisals. Their salary grows with their performance rating. As a PSU employee, that’s not how your pay works. Your basic pay moves slowly — usually only after a Pay Commission revision, which happens once in years. So the government created DA to make sure your salary keeps up with rising prices in the meantime.

DA — Dearness Allowance — is a fixed percentage of your basic pay. It goes up when the cost of living goes up. The calculation is linked to the All India Consumer Price Index, or AICPI. When that index rises, your DA percentage rises too.

For Assam state government and state PSU employees, DA is revised twice a year — once effective January 1 and once effective July 1. That is why every 6 months, there is either a hike announcement or a disappointment. The Assam Cabinet recently approved a 2% hike, taking DA from 58% to 60% of basic pay.

Think of DA as the government’s way of saying — we cannot give you a raise every year, but we will not let inflation eat your salary either. The problem is, most PSU employees treat every DA hike as found money. And found money, as you already know, has a way of disappearing fast.

How Much Extra Money Are We Actually Talking About?

Let us put a real number to this so it stops feeling abstract.

Take a PSU employee with a basic pay of ₹40,000 per month. A 2% DA hike means ₹800 more per month on paper. After standard deductions — PF contribution, professional tax, and other cuts — the actual amount landing in hand is roughly ₹700 per month. Not a life-changing number on its own.

But here is where it gets interesting. DA hikes almost always come with arrears. The revised rate is effective from an earlier date — usually 3 to 4 months back. So in the month the hike is paid out, you are not just getting ₹700 extra. You are getting ₹2,100 to ₹2,800 in one shot, quietly mixed into your regular salary.

That lump sum is real money. For many PSU employees it is the biggest unexpected credit they see in months. And because it arrives without fanfare — no separate notification, just a fatter salary slip — most people do not treat it with any intention.

Your pay scale will give you a different number. But the point is the same. A small monthly hike becomes a meaningful lump sum because of arrears. What you decide to do in those first 48 hours after salary credit determines whether that money works for you — or simply disappears.

Where Does the Money Go? (The Honest Answer)

Let us be honest about this. No lectures, no shame — just the truth.

The month DA arrears land, the salary looks bigger. And a bigger salary feels like permission. Groceries get upgraded. The kids get new clothes or a toy they have been asking for. There is a small family outing. Maybe a new dress or something for the house that has been pending for a while. None of these things are wrong. All of them are completely understandable.

But here is what actually happens. These are not one-time expenses. Groceries upgrade and stay upgraded. The outing becomes a habit. The lifestyle quietly shifts to match the new salary number — and then stays there even after the arrears month is over. This is called lifestyle inflation. And it is the single biggest financial leak in a PSU employee’s life.

The money does not get wasted on one big bad decision. It gets absorbed in dozens of small, reasonable-looking ones. That is what makes it so hard to catch.

I know this because I did the same thing. My DA arrears went straight to EMI payments. Not groceries, not outings — EMIs. It felt responsible. And paying off debt is not a bad move. But I never once stopped to ask — should even a small part of this go somewhere that grows? That question is what this article is really about.

The 60-40 Rule for DA Arrears

The idea is simple. When your DA hike hits your account, do not let it dissolve into your regular expenses. Split it deliberately — 60% goes to investing, 40% goes to your life.

Take the same example. Basic pay ₹40,000. DA hike of 2% gives you roughly ₹700 extra in hand every month. Apply the 60-40 rule — ₹420 goes into your SIP, ₹280 goes wherever it needs to go. Groceries, EMI, an outing — your call. No guilt, no restriction on that 40%.

The reason this works is because you are not asking yourself to sacrifice. You are not cutting anything you currently enjoy. You are only deciding what to do with money you did not have last month. That is the easiest saving decision you will ever make — because you never got used to spending it in the first place.

The 60% does not have to be perfect. If ₹420 feels too tight, start with ₹300. The number matters less than the habit. What matters is that you make a decision before the salary hits — not after. Once the money mixes into your account, it is gone.

This rule works especially well for PSU employees because DA hikes are predictable. They come every 6 months like clockwork. That means every 6 months, you have a fresh opportunity to step up your savings — without touching a single rupee of your existing take-home.

Why Step-Up SIP and DA Hike Are a Perfect Match

Most PSU employees have already figured out how to live on their current salary. The groceries are sorted. The EMIs are running. The monthly expenses have found their level. Life is stable, if not comfortable.

Then DA gets hiked. And almost immediately, the expenses find a way to rise too. A slightly better grocery brand. An extra outing. Something small here, something small there. The salary went up — so the lifestyle goes up to meet it. This is lifestyle inflation, and it happens automatically unless you make a conscious decision to stop it.

Here is the question worth asking. The same groceries that were enough last month — are they suddenly not enough this month? The same household that ran on your previous salary — does it genuinely need more money now? In most cases, the honest answer is no. Nothing changed except the number on your salary slip.

That is exactly why step-up SIP and DA hike are a perfect match for PSU employees. Your lifestyle does not need the extra money. Your future self does. A step-up SIP lets you increase your monthly investment amount at regular intervals — and DA hikes give you a ready, predictable trigger to do exactly that every 6 months.

Central and state PSU employees typically get DA revised twice a year. That means twice a year, you have fresh money arriving that your current lifestyle has not learned to spend yet. If you act in that small window — before the money settles into expenses — you can step up your SIP without feeling a single rupee of pain.

The private sector employee waits for an appraisal that may or may not come. You do not have to. Your step-up schedule is already written into the government calendar.

What About EMIs and Loans — Should You Pay Them Off First?

This is the question most PSU employees never ask clearly. They either throw everything at the loan without thinking, or they ignore the loan and start investing while paying 14% interest somewhere. Both extremes are mistakes.

Here is a simple way to decide. Look at the interest rate on your loan. If you are paying 12% to 15% on a personal loan, that loan is costing you more than most investments will earn you. Paying it off first is not a conservative move — it is the smartest investment you can make. A guaranteed 13% saving beats a probable 12% return any day.

But if your loan is a home loan or a vehicle loan at 6% to 8%, the math flips. A decent equity mutual fund SIP has historically delivered more than that over the long term. In that case, use the 60-40 rule — put 60% of your DA hike into your SIP and use the remaining 40% toward your EMI or daily expenses.

I used my own DA arrears to pay off EMIs. At the time it felt like the responsible thing to do. And if those were high-interest personal loans, it absolutely was. The mistake is not paying off debt — the mistake is never asking whether even a small portion could go toward building something at the same time.

You do not have to choose between debt freedom and wealth building forever. But you do need to know your interest rate before you decide which one comes first.

The One Thing You Must Not Do When DA Hits Your Account

The moment extra money hits your account, there is a natural urge to celebrate. A dinner out. A round of drinks with friends. A small treat for the family. You earned it, the thinking goes — so why not enjoy it?

Here is the problem. A DA hike is not a bonus. It is not a reward for performance. It is a cost-of-living adjustment — money the government is giving you because everything around you is getting more expensive. Spending it on celebration is like getting a medical reimbursement and blowing it on a vacation.

The single worst move you can make when DA hits your account is to treat it as an occasion. One party, one outing, one impulsive purchase — and three months of arrears are gone in a weekend. The salary goes back to feeling normal within days. And the opportunity to step up your SIP, close a loan faster, or build even a small emergency fund simply disappears.

Decide what to do with the money before it arrives. Not after. The moment it mixes into your account without a plan, your expenses will find it before you do. That is not a character flaw — it is just how money works when there is no intention behind it.

One decision, made one day before salary credit, can change where that money goes. That is all it takes.