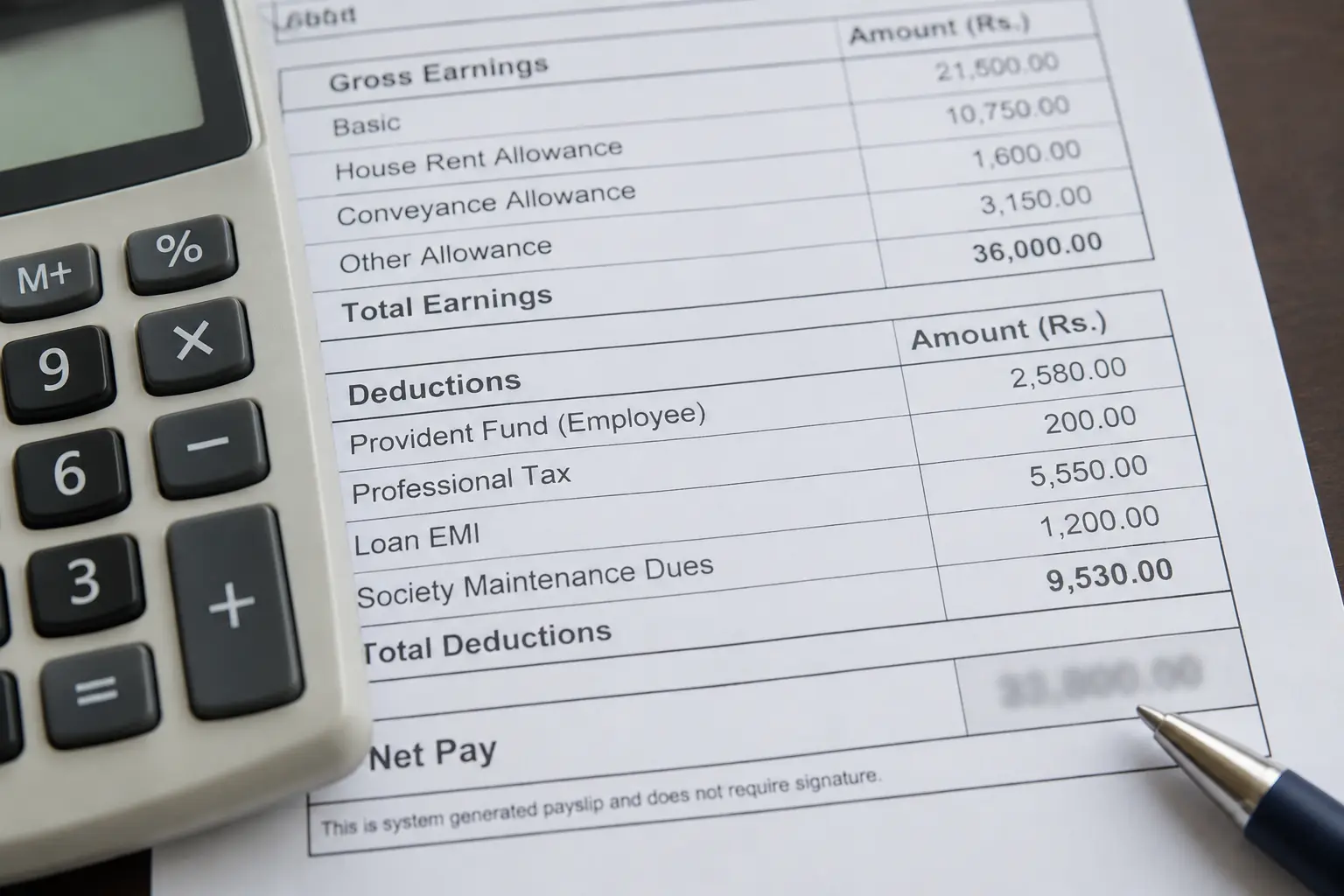

The First Sign: A Salary Slip With Almost Nothing Left

EMI deduction limit PSU employee salary: there isn’t a clean answer, and you only find that out the hard way.

A colleague of mine once opened his salary slip and found a negative number where his net pay should have been. Not a low number. Negative.

He had run out of paid leave that month. Every day of unpaid absence turned into a loss-of-pay deduction, on top of the EMIs and society dues he was already carrying: a home loan, an advance, society expenses. None of those obligations wait for attendance to improve. They come out first, every month, no matter what else is happening in someone’s life.

That month, attendance and obligations collided. Once payroll finished deducting what he owed, there was nothing left. Worse than nothing. HR stepped in and added five hundred rupees, not because any rule required it, but so the account would not actually show a negative balance. It made him break even. Zero, not negative.

The shortfall did not disappear. What payroll could not recover that month got carried forward, and he spent the next cycle repaying the leftover obligations on top of his usual deductions. A hole from one bad month follows you straight into the next one.

This is not a freak case. It is what happens, often quietly, inside PSU payroll systems, and almost nobody outside payroll sees it until it happens to them.

How Payroll Actually Decides What Gets Deducted First

There is an order to this, even if nobody ever explains it to you when you join. The first deductions out are statutory ones: provident fund, tax at source, professional tax, whatever the law requires. These do not wait for anything. They come out before the salary even reaches your bank account, regardless of what is left after.

After the statutory deductions, the next in line are loan EMIs and advances, the money you owe directly to the company or that the company has guaranteed on your behalf, like an HBA recovery. The logic is simple from the employer’s side: the company should never be the one left chasing an employee for a recovery. So this layer gets protected ahead of almost everything else.

Only after that come the softer deductions: society expenses, salary savings schemes, voluntary contributions. These sit last in the queue, which means they are also the first to get squeezed when the math stops working.

Nobody hands you this order on day one. You only learn it the hard way, usually when a month goes wrong and you start asking why one deduction bounced while another did not.

What Happens When One Month’s Salary Can’t Cover the Deductions

When the math does not work, there is no pause button. Nobody from payroll calls to ask whether you would like the EMI deducted next month instead. The system runs its priority order, takes what it can, and whatever it cannot recover that month simply waits.

Waits is the wrong word, though. It does not sit quietly. It gets added to next month’s deductions, on top of whatever is already scheduled to come out then. So a shortfall in March does not stay a March problem. It becomes a heavier April, and if April cannot absorb it either, a heavier May.

This is not written down anywhere that I have seen. No circular, no service rule spells out “deferred deductions carry forward and compound.” It is just how the system behaves in practice, learned by watching it happen rather than reading it in a document. Treat it as common payroll-floor behavior, not a legal guarantee, because what one PSU’s payroll software does is not necessarily what another’s does.

What this means in plain terms: one bad month rarely costs you one bad month. It costs you the next one too, a little worse, until either your situation improves or the obligations themselves come down.

The 50% Deduction Cap Under the New Wage Code, and the Catch for PSU Employees

In November 2025, the rules around salary deductions actually changed, though almost nobody noticed. The Code on Wages, 2019 replaced the old Payment of Wages Act, and under Section 18 of the new Code, total deductions from your wages in any wage period cannot exceed 50 percent. That is a real number in a real law, not a rule of thumb someone made up.

This is actually an improvement over the old position. The Payment of Wages Act allowed deductions up to 75 percent in certain cases, mainly where cooperative society dues were involved, which is exactly the kind of deduction many PSU employees carry. The new Code does away with that carve-out, at least on paper.

Here is the catch. Section 25 of the same Code says this protection does not automatically apply to what the law calls a “Government establishment,” unless the government specifically notifies that it should. A Government establishment, in the legal sense, means an office or department of the government.

Most PSUs are companies, not literally an office of the government, even though they are government owned. Whether that 50 percent cap technically binds your PSU’s payroll, or whether your PSU falls outside it the way a government department might, is genuinely unsettled, and I am not going to pretend otherwise. It depends on how your specific PSU is incorporated and whether any notification has been issued covering it, something worth actually asking your HR or finance department about, rather than assuming either way.

What I can tell you is what I already showed you in the first section. The colleague whose salary went negative was not protected by any 50 percent floor. Whatever the law says on paper, the practice on the ground, at least at this PSU, has not been built around that cap.

It helps to know what Section 18(2) actually allows in the first place. The list includes fines, deductions for absence from duty, damage or loss caused by negligence, house accommodation and similar amenities, recovery of advances, recovery of loans including house-building loans, income tax, and contributions to a cooperative society or welfare fund, among a few others.

Almost every deduction a PSU employee actually sees on a payslip, like PF, HBA recovery, society dues, or an advance, falls somewhere in that list. The 50 percent cap applies to all of them added together, not to each one separately.

On the “appropriate Government” question, at least one piece of this is settled. The Code itself defines, in Section 2, that for an establishment that is a central public sector undertaking, the appropriate Government is the Central Government. So if your PSU is a central one, it is the Central Government that holds the power to extend Chapter III to Government establishments by notification, not some unnamed authority nobody can pin down.

What remains genuinely open is whether your specific PSU even counts as a “Government establishment” in the first place. That term is defined narrowly, as an office or department of the government, and most PSUs are companies, not departments. If your PSU does not meet that narrow definition, the Section 25 exemption may not apply to it at all, which would mean the 50 percent cap binds it by default.

This is exactly the kind of distinction your own HR or finance department should be able to settle, worth asking about directly rather than assuming either way.

A Different Protection: What Happens If a Bank Takes You to Court Instead

Everything in the last section was about deductions your employer makes directly, the EMI and society dues coming out of payroll. A bank loan default works differently, because the bank is not your employer and cannot simply instruct payroll to deduct anything. If a bank wants to recover money you owe and you are not paying, its real route is to go to court and get an order attaching part of your salary.

Getting to that point is not quick or automatic. A bank cannot walk into your office with a default notice and start deducting your salary. It first has to sue you and win, which means a full civil suit and an actual money decree from a court. Only after that, while trying to execute the decree, can the bank apply under Order 21 of the Code of Civil Procedure to attach a debt owed to you, which is exactly what your employer owing you a salary is in the eyes of the law.

The court then issues a notice to your employer as the garnishee, ordering it to either pay the relevant amount into court or appear and explain why not. If the employer ignores that notice entirely, the court can treat the notice itself as if it were a decree against the employer too. That whole chain, lawsuit, decree, execution, garnishee notice, is why this route takes months or years, not days.

Indian law has actually protected salaries from this for a long time, well before the Code on Wages existed. Under Section 60 of the Code of Civil Procedure, the first one thousand rupees of your salary plus two-thirds of whatever is left above that stays protected.

Only the remaining third of that balance can actually be attached for an ordinary debt decree. For a maintenance decree specifically, that protection flips: only one-third stays exempt, and the court can take the other two-thirds.

That one-thousand-rupee figure has not moved with inflation in a long time, which tells you something about how rarely this provision gets revisited. It was written for a different economy. Treat it as the legal floor that exists on paper, not a number that reflects what one thousand rupees actually means today.

None of this has happened at my PSU, and I want to be honest about that rather than dramatize it. What has happened instead, more than once, is something quieter. The bank tells the office directly: do not extend this person any more credit. No NOC gets issued, which blocks the employee from moving the salary account to another bank.

The same person cannot take a fresh loan from that bank, cannot take one from a different bank either, once the default shows up, and cannot take a company loan or advance. It stays at that level for now. Whether it escalates to an actual court order is a real possibility, just not something I have seen happen yet.

What Is the EMI Deduction Limit PSU Employee Salary?

Not really, in practice. On paper, the Code on Wages caps deductions at 50 percent, but whether that legally binds your PSU depends on the Government establishment question above, and even where the cap clearly applies, it is a ceiling on deductions, not a promise that what’s left is enough to live on.

What should you do if your deductions already cross 50 percent of your salary?

Talk to your payroll or finance section honestly, before a month actually goes negative. Ask specifically how your office handles overflow, whether it defers and stacks the way I described, or whether there’s a formal restructuring option, since this varies by PSU and no general article can answer it for you.

Can a bank directly order your employer to deduct an EMI from your salary?

No, not unless you’ve personally authorized a standing instruction or NACH mandate for it. A bank’s only forcible route without your consent is a court and a garnishee order, which takes months. What banks do without going to court, and what actually pinches first, is deny a fresh loan or NOC and blacklist you informally.

The Real Lesson: Why Margin Matters More Than the Size of the Mistake

The pattern I keep seeing on the payroll side is not really about how someone got into debt. It is about how little room a PSU salary leaves for getting back out. Statutory deductions go first, no matter what. Loan EMIs and advances go next, because the company protects its own recovery before anything else. Whatever is left over has to cover everything else in your life. For a lot of PSU employees, that leftover is thin even in a good month.

That thinness is the actual danger, not any one bad decision. A small slip, a missed EMI, an unplanned expense, a month with too much unpaid leave, does not stay small. It collides with deductions that refuse to wait, gets deferred into the next month, and compounds from there.

The 50 percent cap under the new wage code may or may not even apply to your PSU on paper, and the court-attachment protection under the Code of Civil Procedure only shows up once a bank has already given up on you and gone to court. Neither one stops the squeeze while it is happening.

If there is one thing worth taking from all of this, it is that wealth does not come from a clever shortcut. It comes from knowledge, applied patiently, before you take on the next obligation rather than after. Most of the damage I have described in this piece did not happen because someone made one dramatic mistake. It happened because the margin was already too thin to absorb anything going wrong, and something eventually did.

So before you sign up for one more EMI, advance, or society scheme, do the arithmetic that nobody at the office will do for you. Add up everything already committed against your gross salary. If that number is already close to half, you are not one bad month away from trouble. You are already in it, you just have not seen the slip yet.