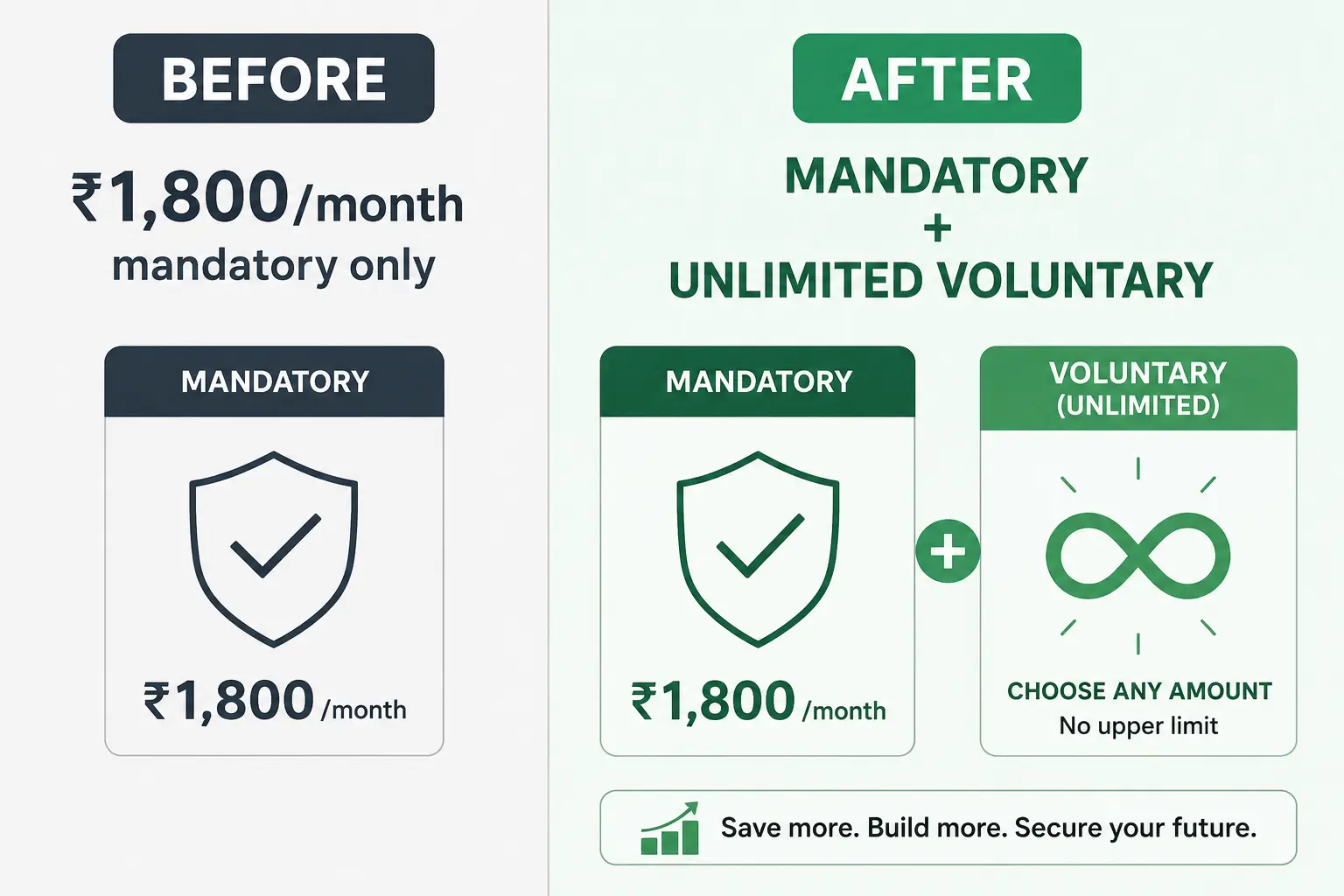

What Changed: EPFO’s New Voluntary PF Contribution Rule

If you’re covered under EPFO, something changed for you on 29th June 2026. The government notified the new EPF Scheme, 2026, replacing the old 1952 scheme. One part of this update matters a lot more than it sounds: employees can now voluntarily contribute above the mandatory PF deduction, and there’s no compulsion or restriction on how much extra you put in. (If you need a refresher on how EPF, EPS and EPFO actually work, I’ve covered the basics here.)

Till now, the mandatory contribution stayed capped at ₹1,800 a month, which is 12% of the ₹15,000 wage ceiling, regardless of what your actual basic pay was. Anything beyond that needed a separate Voluntary Provident Fund arrangement. Under the new scheme, this voluntary route is formally opened up and simplified.

For PSU employees like us, this sounds like good news on the surface. More retirement savings, same safe EPFO umbrella, no new paperwork headache. But there’s a catch buried in the tax rules: PF interest taxable above 2.5 lakh is a real thing, and this new voluntary window makes it reachable for people who never had to think about it before.

I got to know about this notification only a few days ago myself. Being freshly issued, it hasn’t spread widely yet among PSU staff, and most of my colleagues have no idea it exists. That gap between the rule changing and people finding out about it is exactly where the risk sits, since decisions about VPF often get made before anyone has checked the tax angle.

Why PF Interest Taxable Above 2.5 Lakh Is Suddenly a Real Risk

Here’s the part that doesn’t get talked about enough. Since 2021, interest earned on your own PF contribution above ₹2.5 lakh in a financial year has been taxable. This rule already existed.

It just never applied to most PSU employees like us, because our mandatory contribution was capped at ₹1,800 a month, which comes to ₹21,600 a year. Nowhere close to ₹2.5 lakh. That safety net is gone the moment you opt for extra voluntary contribution.

If you’re the kind of saver who likes to put money in a “safe government scheme” and forget about it, this new voluntary window can quietly push you past the threshold without you realizing it. The risk isn’t really about high earners chasing bigger PF balances.

It’s about cautious savers who assume PF is fully tax-free no matter how much they put in. That assumption stopped being true years ago for the amount above ₹2.5 lakh, and now more people can actually reach that number.

The ₹2.5 Lakh Limit Explained: EPFO vs Government Employees

There’s some confusion worth clearing up here, because I’ve seen this trip people up. Government employees under the old Statutory Provident Fund get a higher exemption limit of ₹5 lakh, not ₹2.5 lakh. That higher limit applies specifically where the employer does not contribute to the fund.

PSU employees, including those of us at State PSUs, are usually covered under EPFO, not SPF. Since EPFO accounts do get an employer contribution matching ours, the exemption limit for us stays at ₹2.5 lakh, not ₹5 lakh. This distinction matters because “government employee” gets used loosely, and someone might assume the higher limit applies to them when it doesn’t.

People sometimes lump “PSU employee” and “government employee” into the same tax bracket in their head, especially when discussing retirement benefits. It’s an easy mix-up. PSU employees usually sit closer to private-sector EPFO rules for PF purposes, even though the job itself carries a public-sector, government-linked identity in every other sense.

If your PF is deducted through EPFO, as it is at my organization, plan around the ₹2.5 lakh figure. Do not assume the government-employee exemption applies to you. When in doubt, check your PF passbook or your Form 26AS, since the taxable and non-taxable portions are meant to be tracked separately from FY 2021-22 onward.

How Much VPF Actually Pushes You Past the Threshold

The mandatory EPF contribution stays fixed at ₹1,800 a month, or ₹21,600 a year. To cross ₹2.5 lakh in total employee contribution for the year, you’d need to add roughly ₹19,000 or more a month in voluntary contribution on top of that.

This isn’t about your basic pay slab anymore. Under the old rules, higher basic pay meant higher mandatory PF automatically. Now the mandatory part is capped for everyone, so crossing the threshold depends entirely on how much you choose to voluntarily set aside, not what you earn.

That’s exactly why the cautious saver is more at risk here than the big spender. Someone earning a modest salary who decides to route a large chunk of savings into VPF, thinking of it as a safe, tax-free option, can hit this limit just as easily as someone earning much more. A person earning ₹40,000 basic who adds a large voluntary amount can cross the line faster than a person earning double that but contributing conservatively.

TDS on Your PF Interest: What Gets Deducted and Where It Shows Up

Once your PF contribution crosses ₹2.5 lakh in a year, EPFO doesn’t wait for you to declare the interest yourself. It deducts TDS directly at 10% on the taxable portion of your interest, under Section 194A of the Income Tax Act. This only kicks in once that taxable interest crosses ₹5,000 for the year.

EPFO maintains two separate accounts for you internally, one for the non-taxable contribution up to ₹2.5 lakh, and one for the amount above it. Interest earned on the taxable account gets added to your income under “Income from Other Sources” and taxed at your slab rate, with the TDS already deducted adjusted against it.

If your PAN isn’t linked to your PF account, the TDS rate jumps to 20% instead of 10%. This is one more reason to make sure your PAN and UAN are properly linked, since a small paperwork gap can quietly cost you more in tax.

A Simple Example of PF Interest Taxable Above 2.5 Lakh in Practice

Let’s say your mandatory PF contribution is ₹1,800 a month, which is ₹21,600 a year. You decide to add ₹20,000 a month as voluntary contribution, taking your total employee contribution to ₹2,61,600 for the year. That’s ₹11,600 above the ₹2.5 lakh limit.

At the current EPF interest rate of 8.25% for FY 2025-26, the interest earned on that excess ₹11,600 works out to roughly ₹957 for the year. Since this falls below the ₹5,000 threshold for TDS, no tax would actually be deducted at source in this specific case.

Push the voluntary contribution higher, say ₹35,000 a month, and your total contribution jumps to ₹4,21,600, which is ₹1,71,600 above the limit. Interest on that excess would come to around ₹14,157, well past the ₹5,000 mark, triggering a 10% TDS deduction of about ₹1,416.

The gap between “barely taxable” and “meaningfully taxable” can come down to just a few thousand rupees of monthly VPF decision. This is exactly why doing the arithmetic before opting in matters more than it seems.

Neither of these numbers is large enough to change your decision to contribute. But they show how quickly the taxable interest scales once you cross the ₹5,000 TDS threshold, and why a rough back-of-envelope calculation before you fix your monthly VPF amount is worth five minutes of your time.

Should You Still Opt for VPF? Weighing the Real Return

None of this means VPF is a bad idea. Even after the taxable portion is accounted for, EPF interest at 8.25% is still one of the safest returns available anywhere, and the taxable slice only applies to the excess above ₹2.5 lakh, not your entire contribution.

The real question is whether you’re choosing VPF deliberately or defaulting into it because it feels safe and familiar. If you already have other tax-saving instruments filled up and want a low-risk parking spot for extra savings, VPF still makes sense even with some interest taxed at your slab rate.

Where it stops making sense is when someone assumes the entire return is tax-free and plans their retirement corpus on that wrong number. A taxed 8.25% is still solid, but it’s not the same figure you’d get if none of it was taxed, and that gap should factor into how much you actually voluntarily contribute.

It also helps to compare VPF against your other available options before committing a large monthly figure. PPF interest remains fully tax-free regardless of amount, though it comes with its own annual contribution cap and a longer lock-in. Equity-linked options can offer higher long-term returns but carry market risk that VPF simply does not have.

There’s no universally right answer here. A risk-averse PSU employee nearing retirement might still prefer VPF despite the partial tax hit, purely for the certainty. A younger employee with a longer investment horizon might choose to split extra savings between VPF and equity instead of pushing everything into one safe basket.

The point of understanding PF interest taxable above 2.5 lakh isn’t to scare you away from VPF. It’s to make sure the number you see in your retirement projection is the actual post-tax number, not an inflated one that assumes every rupee of interest stays tax-free forever.

What PSU Employees Should Do Before Opting In

Before you sign up for extra voluntary contribution, do the basic math first. Check your current mandatory contribution, decide how much extra you’re comfortable adding, and estimate whether that total will cross ₹2.5 lakh for the year.

This isn’t complicated arithmetic, but very few people actually sit down and do it. If you’re already close to or above the threshold, that doesn’t mean stop contributing.

It just means going in with clear eyes about which portion of your interest will be taxed, rather than assuming the whole thing stays tax-free the way it might have felt before this new scheme opened things up. I am not a SEBI-registered advisor or a CA, and views expressed are personal.

If your VPF decision is a large one, it’s worth running the numbers past your own accounts office or a tax professional before you commit to a fixed monthly figure. A ten-minute calculation now can save you from a confusing TDS entry in your Form 26AS a year later.

This new voluntary window is a genuine opportunity for PSU employees to build a larger, safe retirement corpus, something that wasn’t easily available to us before. Just walk into it with the ₹2.5 lakh figure in mind, so the tax outcome matches what you actually expected going in.

FAQ

Is the new voluntary PF rule mandatory for PSU employees?

No. Opting for extra voluntary contribution is entirely your choice. Your employer is not required to match it, and you can start, reduce, or stop it whenever you want.

Will my entire PF interest be taxed if I cross 2.5 lakh?

No. Only the interest earned on the portion of your contribution above ₹2.5 lakh is taxable. Interest on the contribution up to ₹2.5 lakh remains fully tax-free, as it always has.

Does the employer’s contribution count toward the 2.5 lakh limit?

No. The limit applies only to your own employee contribution, including any voluntary amount. Employer contributions are tracked separately and are not counted toward this threshold.

How will I know if TDS has been deducted on my PF interest?

It should reflect in Form 26AS and AIS, along with a Form 16A issued for the TDS amount. If it isn’t showing up despite crossing the threshold, it’s worth checking with EPFO or your PF trust directly.

Does this new voluntary PF rule change anything for existing VPF subscribers?

No. If you were already contributing to VPF before this notification, nothing changes for your existing arrangement. The June 2026 update simplifies and formalizes the voluntary contribution route for everyone, but the 2.5 lakh taxable-interest rule has applied to VPF contributions since 2021 regardless.

Can I stop my voluntary PF contribution once I start it?

Yes. Voluntary contributions are not locked in. You can reduce or stop the additional amount whenever you choose, without affecting your mandatory EPF contribution, which continues as usual.