The FD to Mutual Fund Shift I’m Seeing on My Own Desk This ITR Season

This ITR season, I noticed something I couldn’t ignore while sitting at my own laptop filing returns. I run a small, informal tax filing practice under my wife’s name, no legal obligation attached, just something I do for colleagues and their families who trust me with the numbers. A couple of years back, most of the returns I filed were ITR-1. Simple salary, maybe an FD or two, nothing that needed a capital gains schedule.

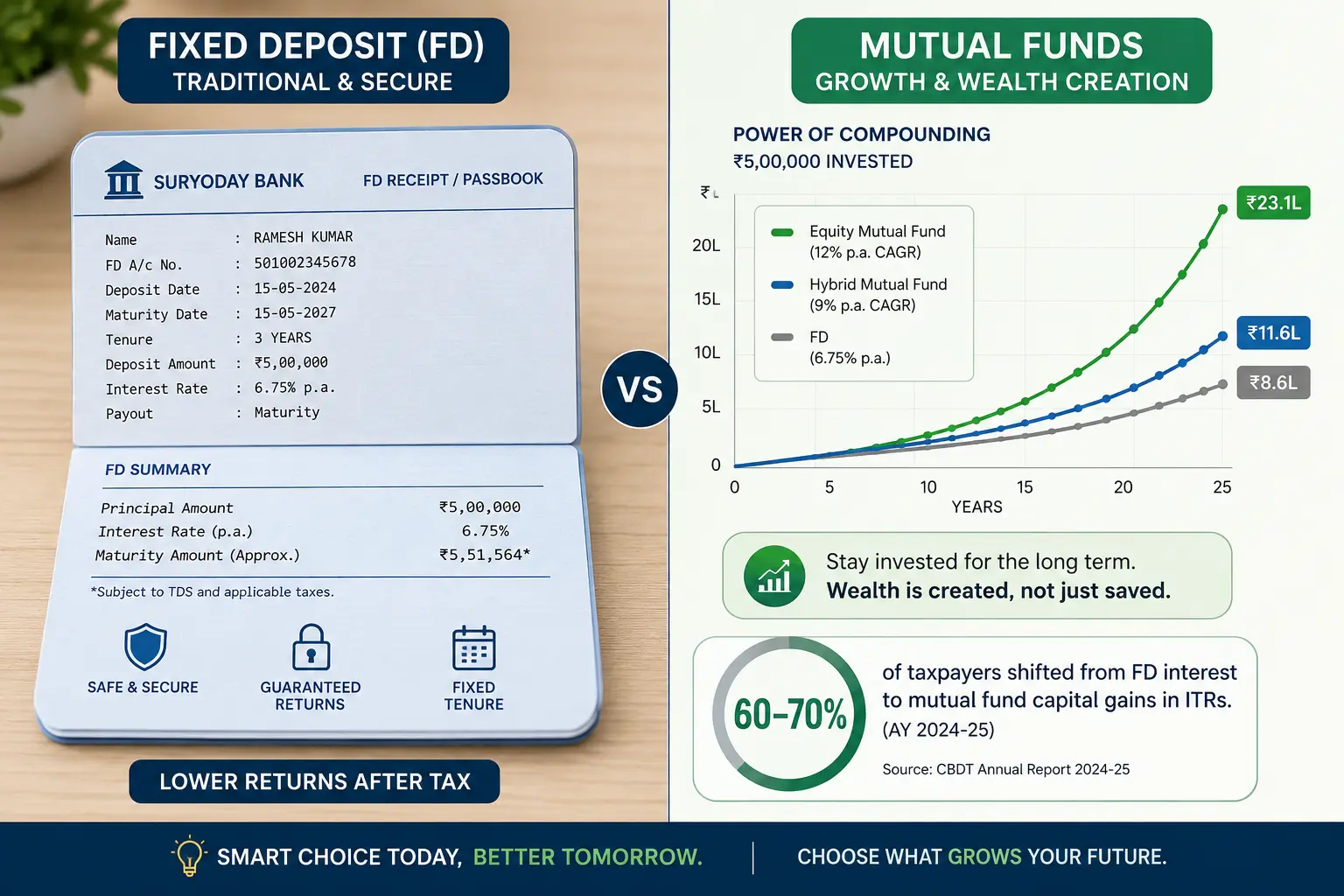

This year, that pattern has flipped. Out of roughly 100 returns I’ve filed this season, I’d estimate 60 to 70 percent needed ITR-2 or ITR-3, not because people changed jobs or started businesses, but because they had mutual fund transactions to report. What I’m watching, client after client, is the FD to mutual fund shift happening in real time, not as a headline trend but as a pattern sitting in actual tax filings.

I am not a SEBI-registered advisor or a CA, and views expressed are personal. But I do sit in a seat that most financial writers don’t: I see the actual tax filings, not just what people say they invest in. That gap between what people claim and what their capital gains schedule shows is where this article comes from.

Why PSU Employees Traditionally Trusted FD and RD Over Everything Else

To understand why the shift I’m seeing now is significant, you have to understand what came before it. Most PSU and government employees grow up financially inside a system built entirely around guaranteed, government-backed instruments. GPF, PF, pension: every major retirement product we’re handed at work is safe, fixed, and government-guaranteed. It’s natural that this becomes the mental template for what “correct” investing looks like.

FD and RD fit that template perfectly. They came from a bank, carried a fixed, printed interest rate, and required no research, no market-watching, and no risk of loss. For a large part of the last two decades, they were also genuinely competitive. Before 2020, FD rates of 7 to 8 percent were common, so the “safe” choice didn’t even feel like it was sacrificing much return.

There’s also a structural piece to this. A PSU salary is stable and predictable in a way that most private-sector income isn’t. That stability removes the urgency that pushes people in less secure jobs to actively chase better returns. When your job itself feels like the biggest financial decision you’ve already gotten right, FD and RD become less of a strategy and more of a default you never revisit.

This is exactly what my old ITR-1 filings reflected. Salary income, a little FD interest, nothing else. No capital gains schedule, because there was nothing to report.

What Changed: COVID-Era Rates and the Mutual Fund Boom

The break from the FD default didn’t happen gradually. It happened because two things collided at once. First, FD rates fell off a cliff during the COVID period, dropping well below what most people had come to expect from a “safe” bank deposit. Suddenly the instrument that had justified itself on returns for two decades wasn’t returning much at all.

Second, equity markets did the opposite. After the initial 2020 crash, markets ran up hard, and anyone who put money into equity mutual funds during that window, even nervously, saw real, visible gains within a year or two. That combination is what actually broke the habit: not a sudden change in risk appetite, but FD becoming genuinely unattractive at the exact moment mutual funds became genuinely rewarding.

Once a few people in any office see a colleague’s mutual fund statement outperforming their own FD renewal, word travels fast. That’s not financial literacy content doing the work. That’s peer proof, and in a stable, tight-knit PSU workplace, peer proof spreads faster than any advisor’s pitch ever could.

This wasn’t happening in isolation either. The same period saw a broader wave of financial content and mutual fund awareness reach far more people than before, which meant the peer conversations happening in PSU offices had backup: articles, calculators, and comparisons that made the shift feel less like a gamble and more like catching up.

The Colleague I Convinced to Make the Shift

One conversation stands out because I was the one who pushed it. A colleague of mine kept renewing FDs year after year, treating it as the obvious, responsible choice. I sat with him and walked through the actual math: his FD interest was being added straight to his taxable income and taxed at his slab rate, and after adjusting for real-world inflation, the money wasn’t growing so much as standing still.

I showed him the other side too. Equity mutual funds held long-term get taxed far more gently, at a flat 12.5 percent on gains above ₹1.25 lakh a year, with no slab-rate erosion. That difference alone changes the entire post-tax outcome over a working career, not because FD is a bad product, but because it was never built to fight inflation and today’s tax treatment the way equity is.

He wasn’t fully convinced in one sitting. But he started small, moved a portion of what would have gone into his next FD renewal into a mutual fund instead, and kept the rest where it was. That’s the shift I keep seeing repeated across my client base this ITR season: not people abandoning FD entirely, but people finally questioning a habit they’d never questioned before.

The Real FD to Mutual Fund Math: Tax, Inflation and Long-Term Returns Compared

Here’s the comparison I actually walked my colleague through, stripped of jargon. FD interest is added to your total income and taxed at your slab rate, which for most PSU employees in mid-career grades means 20 to 30 percent of every rupee of interest earned. Equity mutual fund gains held over a year are taxed far more gently: 12.5 percent on long-term gains above ₹1.25 lakh in a year, with nothing owed below that threshold.

| Fixed Deposit | Equity Mutual Fund (Long-Term) | |

|---|---|---|

| Typical rate assumed | 7% per year | 12% per year (realistic long-term average, not guaranteed) |

| Tax treatment | Added to income, taxed at slab rate | 12.5% LTCG above ₹1.25 lakh/year |

| Inflation impact | Often barely beats or loses to inflation after tax | More likely to outpace inflation over 10+ years |

| Volatility | None, fixed and predictable | Real, year-to-year value can fall |

Put real numbers on it. Assume you put ₹5 lakh into an FD at 7 percent for ten years versus the same ₹5 lakh into an equity mutual fund at a realistic 12 percent long-term average. The FD, taxed every year at a 30 percent slab rate on the interest, ends up compounding closer to 4.9 percent after tax, and inflation running near 5 to 6 percent a year can wipe out most of that real gain.

The equity investment, taxed only once you sell and only at 12.5 percent above the ₹1.25 lakh exemption, keeps far more of its headline growth intact. Over ten years, that gap isn’t a rounding error, it’s the difference between money that barely holds its value and money that actually builds wealth.

This math only holds if you actually stay invested for the long term. Pull the same money out within a year and short-term capital gains on equity are taxed at 20 percent, which erodes a chunk of the advantage. The 12 percent comparison assumes a horizon of seven to ten years, not a quick in-and-out trade.

The 12 percent figure is a realistic long-term average for equity, not a promise. Mutual funds can and do fall in value in any given year, sometimes sharply, and nobody should move money into them expecting a straight line up. The difference this table shows isn’t “FD is bad,” it’s that FD’s fixed, taxed-at-slab-rate return has historically struggled to beat inflation once tax is accounted for, while equity’s long-term average has a real chance of doing so, in exchange for accepting short-term ups and downs.

This is the exact math I put in front of my colleague. Not a sales pitch, just his own FD renewal slip next to what the same amount would have looked like in an equity fund over the same stretch, after tax, after inflation.oked like in an equity fund over the same stretch, after tax, after inflation.

The Colleague Who Waited Until Near Retirement, and Still Came Out Ahead

Not every mutual fund story I’ve seen belongs to someone young with decades to recover from a bad year. One colleague nearing retirement put a lump sum into equity mutual funds during the COVID-era market dip, at a point when most people were pulling money out of everything, not putting it in. It felt like the riskiest possible move for someone that close to the end of a career.

It worked out well. That lump sum has grown into a meaningful profit, sitting far ahead of what the same amount would have earned sitting in an FD over the same stretch. I want to be honest about why: entering during a sharp dip and staying invested through a strong recovery is not a repeatable strategy, it’s a specific window that happened to work.

The real lesson isn’t “put your retirement corpus into equity funds.” It’s the opposite caution: someone that close to retirement carries real sequencing risk, where a market fall in the wrong year can do serious damage to money you can’t afford to leave invested for another decade. This colleague got the timing right, but I wouldn’t build advice for others near retirement around getting that lucky twice.

How to Make the FD to Mutual Fund Shift Without Overexposing Yourself

None of this means emptying every FD you have into equity mutual funds next week. That would be trading one kind of carelessness for another. The first thing to get right is your emergency fund: 6 to 12 months of expenses in something liquid and safe, FD or a savings account, before a single extra rupee goes into equity. That money is not investment capital, it’s insurance against a bad month.

Past that, the shift works better staggered than sudden. Moving a large lump sum into equity all at once means your entire outcome depends on what the market happens to do right after you invest. Redirecting fresh money, like what would have gone into your next FD renewal, into a SIP each month spreads that risk out and removes the guesswork of timing.

It’s also worth being honest that mutual funds are not a strictly better version of FD. They carry real volatility, and a bad year can mean a visible drop in value, not just a slower gain. The 12 percent long-term average that makes the math work assumes you stay invested through those bad years instead of pulling out when they happen. If you can’t sit through a 15 to 20 percent dip without panicking, that’s information about how much of your money belongs in equity, not a reason to avoid it entirely.

A reasonable starting point for most PSU employees is to keep existing FDs for near-term goals and stability, and direct new savings into equity mutual funds through SIPs for anything more than 5 to 7 years away.

One more habit worth building: review this allocation once a year, not every month. Checking a mutual fund’s value daily during a market dip is the fastest way to panic and sell at the worst possible time. An annual check, ideally around the same time you’re already looking at your FD renewals, is enough to course-correct without letting short-term noise drive long-term decisions.

What I Tell My PSU Clients Before They Switch

Every client who asks me about this gets the same starting point: understand what you’re actually holding before you touch it. FD isn’t a mistake, it’s a tool that’s best for money you need in the next one to three years, not money meant to grow for fifteen. The mistake isn’t owning FD, it’s owning only FD for decades because switching never felt necessary.

The shift I’m watching happen across my ITR filings this season isn’t a fad. It’s roughly two-thirds of my client base now generating capital gains, up from a base that was almost entirely ITR-1 salary-and-FD-interest returns not long ago. That’s not a trend piece, that’s what showed up in the tax forms I filed with my own hands.

If you want the same starting point I gave my colleague, begin with your existing FD renewal slip and honestly compare its post-tax, post-inflation return against a long-term equity average of 12 percent, taxed at the current 12.5 percent LTCG rate. You can read the official rules on capital gains taxation directly from the Income Tax Department. If you’re earlier in your investing journey and want the fundamentals first, my full guide on how to invest your PSU salary is the right place to start.

I am not a SEBI-registered advisor or a CA, and views expressed are personal. What I am is the person who has now filed both versions of your colleagues’ returns, the FD-only kind and the mutual-fund kind, and seen which one is actually working better.