If You’re Still Buying ELSS Every March, Read This First

If you’re still putting money into an ELSS fund every March out of habit, there’s a good chance it isn’t doing what you think it’s doing. For years, the pitch was simple: invest in ELSS, get a Section 80C deduction, and earn equity returns on top. That pitch made sense when almost everyone filed under the old tax regime. ELSS tax saving for PSU employees was built entirely on that old-regime assumption for over a decade, and the assumption quietly stopped holding for most people without anyone flagging it.

Most PSU employees I’ve filed returns for over the last few years have quietly moved to the new tax regime, where Section 80C doesn’t apply at all. If that’s you, the ELSS fund sitting in your portfolio still earns market returns, but it stopped saving you a single rupee in tax the day you switched regimes. Nobody sends a notification for that. You just keep buying the same fund every year assuming the old math still works.

I am not a SEBI-registered advisor or a CA, and views expressed are personal. But this is the exact gap I see most often when reviewing client documents: an ELSS SIP still running on autopilot, years after the tax reason for holding it quietly disappeared.

This isn’t about whether ELSS is a bad fund. It’s about whether you’re holding it for the right reason anymore. That answer depends entirely on which regime you’re actually filing under this year, and that’s where most of the confusion starts.

I see this gap most clearly during tax season, when clients hand me their investment statements alongside their salary slips. The ELSS entry is almost always there, sitting quietly among PPF and insurance premiums, treated as one more line in the same 80C bucket it always belonged to. Nobody questions it because nobody has a reason to, until the regime they actually filed under gets checked line by line against what they’re claiming.

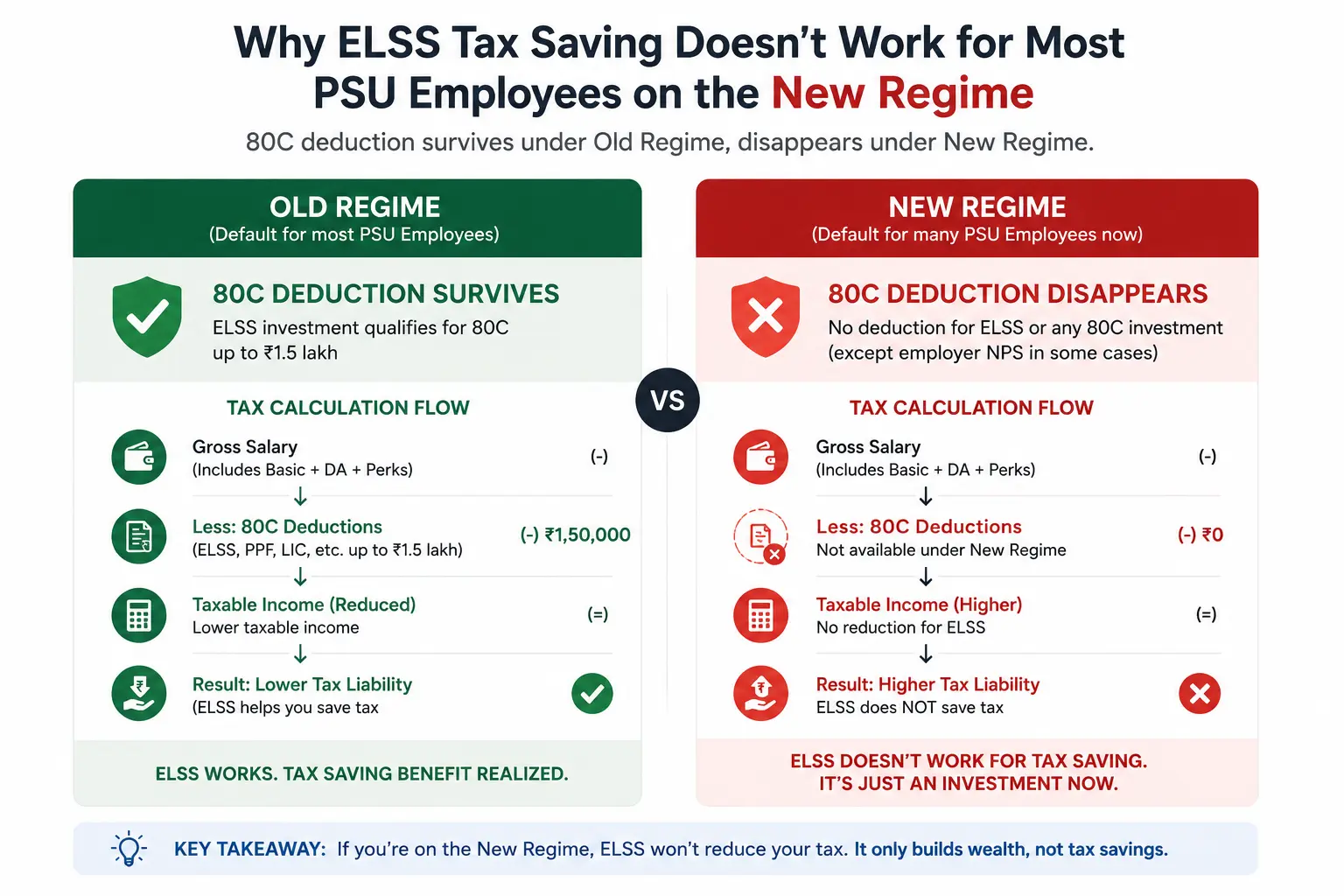

Why ELSS Tax Saving Doesn’t Work for Most PSU Employees on the New Regime

The new tax regime is now the default option for individual taxpayers, and per the Income Tax Department’s own FAQ, Section 80C simply doesn’t exist under it, apart from a narrow set of exceptions like the employer’s NPS contribution.”. That means every rupee you put into ELSS, PPF, or any other 80C instrument earns zero tax benefit if you’re filing under the new regime. The fund itself doesn’t change. Only the reason you originally bought it disappears.

Here’s where I see the actual gap in my own filing practice. Most PSU employees I work with have already shifted to the new regime, mainly because the tax slabs work out better for them without needing to chase deductions. But the ELSS SIP started years ago, back when the old regime was still standard, often keeps running unchanged.

Nobody actively decided to keep it for tax saving. It just never got reviewed. This matters because ELSS carries a 3-year lock-in, and unlike a regular equity fund, you can’t touch it early even if you realize the tax reason is gone.

If you’re already in the new regime and you started an ELSS SIP two years ago, that money is still locked for another year, earning market returns with no deduction attached. That’s not a disaster, but it does mean you were never actually saving tax on it in the first place. You should stop assuming otherwise.

The practical test is simple: check which regime you filed under last year. If it was the new regime, your ELSS contributions have not reduced your tax bill, regardless of how much you’re putting in every month, and no amount of continuing the SIP changes that fact.

Consider the actual numbers for a moment. Say you’ve been running a ₹5,000 monthly ELSS SIP for the past two years under the new regime. That’s ₹1.2 lakh invested with the specific expectation, somewhere in the back of your mind, that it’s helping your tax bill.

It isn’t, and it hasn’t been since the day you switched regimes. The equity returns are real. The tax benefit you assumed was there never was. This is precisely the confusion around ELSS tax saving for PSU employees that carries from one regime into another without anyone ever checking whether it survived the switch.

The Old Regime Exception: When HBA Loan Principal and EPF Actually Fill Your 80C Ceiling

There’s a smaller group where this genuinely still applies, and it’s worth being precise about who that actually is. A few of my clients stay on the old regime specifically because they’ve taken an HBA loan, and the interest deduction under home loan provisions is large enough to outweigh the new regime’s lower slabs.

If that’s your situation, Section 80C is still live for you, and ELSS can still reduce your tax bill. But even here, the ceiling fills faster than most people expect, and not from ELSS. Your EPF contribution counts toward the same ₹1.5 lakh limit.

So does the principal portion of your HBA EMI, which is separate from the interest deduction claimed elsewhere. Stack EPF and HBA principal together, and many PSU employees on the old regime are already close to the ₹1.5 lakh ceiling before any ELSS money enters the picture.

This is the calculation almost nobody runs. You know your EPF deduction from your salary slip, and you know your EMI breakup shows an interest and principal split. Add the two 80C components together first.

Whatever room is left after that is the only portion where an additional ELSS investment actually buys you a deduction, and for many old-regime employees with an HBA loan, that room is smaller than they assume. Take a rough example: an EPF deduction of ₹60,000 a year plus an HBA principal component of ₹70,000 a year already totals ₹1.3 lakh, leaving only ₹20,000 of real 80C room left over. An ELSS SIP beyond that point is still a fine investment, but it isn’t buying any additional deduction.

If you’re on the old regime without a home loan, EPF alone is unlikely to fill the ceiling on a typical PSU salary, and ELSS still earns its keep as a genuine 80C tool. The distinction that matters isn’t old regime versus new regime alone. It’s whether your existing deductions, not ELSS, have already done most of the work.

This is exactly the calculation that separates real ELSS tax saving for PSU employees from the version that quietly stopped applying years ago. A salary slip and an EMI statement are the only two documents you need, and most people already have both sitting in a folder somewhere without ever placing them side by side.

ELSS Tax Saving for PSU Employees: Which Regime It Still Works For

Putting the last two sections together, the question of whether ELSS tax saving for PSU employees still applies comes down to a two-question check, not a blanket yes or no. First, which regime are you actually filing under this year, not which one you started under years ago.

Second, if you’re on the old regime, has your EPF plus HBA principal, if you have a home loan, already used up most or all of your ₹1.5 lakh 80C limit. Answering both honestly takes less time than most people assume, and it’s the only way to know for certain whether your ELSS SIP is still doing what you think it’s doing.

If you’re on the new regime, the answer is straightforward. ELSS gives you zero tax benefit, full stop, regardless of amount invested. The new regime lets you claim the standard deduction and the employer’s NPS contribution under Section 80CCD(2), but the larger deductions like 80C, 80D, HRA, and home loan interest are gone.

There’s no version of the new regime where ELSS buys you a deduction, no matter how the fund itself performs. If you’re on the old regime and carrying an HBA loan, run the actual numbers before assuming ELSS is still useful. Pull your EPF deduction from your salary slip and your EMI principal component from your loan statement.

Add them together against the ₹1.5 lakh ceiling. If there’s meaningful room left, ELSS still earns its 80C benefit for you. If there isn’t, you’re in the same position as a new-regime employee: any further ELSS investment is just an equity fund purchase with no tax angle attached.

Good investments stay good even when the tax wrapper changes, which brings us to the actual question worth asking once the deduction is off the table entirely.

Once Tax Saving Is Off the Table, Is ELSS Still a Good Investment?

Strip away the 80C angle, and ELSS has to be judged the same way as any other equity fund: on returns, consistency, and fit for your goals. On that basis, it’s a reasonable fund, not a standout one. The 3-year lock-in that once looked like a minor inconvenience next to a tax deduction now looks like a genuine limitation with nothing offsetting it. You’re accepting reduced liquidity for no corresponding benefit if you’re on the new regime or if your old-regime 80C ceiling is already full.

Once the tax reason is gone, ELSS still has real equity growth potential, but you’d hold it for that alone, not for the deduction attached to it. Compare that against a flexi-cap or multi-cap equity fund with no lock-in, similar risk profile, and the same long-term return potential.

For PSU employees who no longer need the 80C angle, a fund with no lock-in gives you the same market exposure with the option to exit or rebalance whenever your situation changes, without waiting out a mandatory hold period. That flexibility matters more than it seems on paper, especially if your income situation, loan status, or regime choice shifts again in a few years.

This doesn’t mean sell an existing ELSS holding the moment its lock-in ends. If the fund itself has performed well, there’s no reason to exit purely because the tax benefit is gone. The mistake isn’t holding ELSS.

It’s continuing to buy new ELSS units every March by habit, assuming a tax benefit that stopped applying the year you switched regimes or the year your other 80C deductions filled the ceiling. That single habit, repeated every tax season without a second look, is the entire problem this article set out to describe.

The fix isn’t complicated, but it does take five minutes you probably haven’t spent yet. Check your regime for the current financial year. If you’re on the old regime, add up your EPF and any HBA principal component against the ₹1.5 lakh ceiling before deciding whether fresh ELSS money still earns you anything beyond market returns.

Run that check once this tax season, and you’ll know for certain whether your ELSS SIP is still doing the job you originally bought it for, or whether it’s quietly become just another equity fund in your portfolio. Either answer is fine, as long as it’s the one you actually chose rather than the one you never got around to checking.

Most PSU employees I meet during filing season have never actually sat down and run this two-question check even once, despite having held the same ELSS SIP for three, five, or sometimes eight years. That’s not a criticism. It’s simply that nobody built the habit of revisiting the assumption once the regime rules shifted underneath it. The five minutes this takes is genuinely the hardest part, not the arithmetic itself.

Payroll and tax rules rarely announce themselves loudly when they change something that used to matter. A regime switch happens quietly through a form you fill once a year, and an old SIP just keeps debiting your account exactly as before. The disconnect between the two is where this entire problem lives, and it’s worth closing that gap once rather than carrying the assumption forward for another filing cycle.

None of this requires switching funds, filing an amendment, or making any dramatic change to your portfolio this week. It just requires an honest look at which regime you’re under and whether your other deductions already did the job ELSS was supposed to do. Once you’ve answered that, you’re no longer guessing about ELSS tax saving for PSU employees every tax season, you actually know where you stand.

For a full walkthrough of how EPF, EPS, and PF contributions interact with your PSU salary structure, our EPF, EPS and EPFO guide breaks down the mechanics your HR department rarely explains clearly.

I am not a SEBI-registered advisor or a CA, and views expressed are personal.