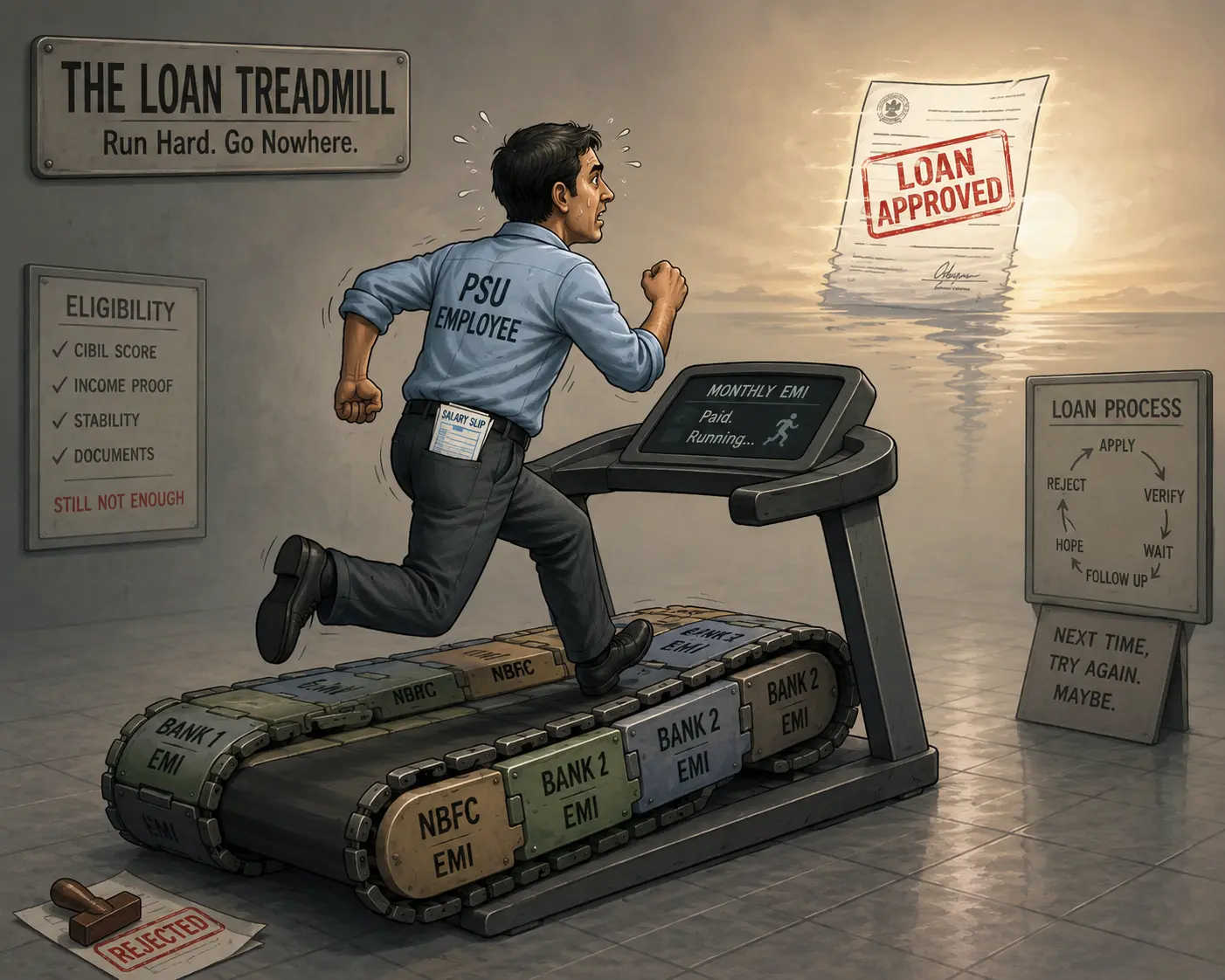

Why Personal Loan Rejection for PSU Employees Doesn’t Make Sense on Paper

If you have a government salary that lands on the same date every month, you’d assume banks are fighting to lend you money. That’s the theory. In practice, a good number of PSU employees walk into a bank or NBFC, salary slip in hand, and walk out rejected.

I’ve seen this up close, both at my desk in the accounts department and through the informal tax filing work I do for colleagues. It’s not a rare glitch. Out of every ten PSU employees who come to me for financial matters, three or four have hit this wall at some point: steady job, steady salary, loan application denied anyway.

Personal loan rejection for PSU employees is rarely random, even though it feels that way to the person holding the rejection letter. There is almost always a specific, identifiable reason sitting underneath it, one that a bank’s internal scoring system caught long before a human ever reviewed the file.

The instinctive reaction is to blame the bank for being unfair to government employees. That’s rarely the real story. The real story sits in three places: a credit score damaged by years of stacking loans, lending practices at some NBFCs that made “low EMI” loans far more expensive than they looked, and a slow-moving cycle of debt that eventually catches up with even the most “secure” salary.

This piece walks through what’s actually happening, using patterns I’ve watched repeat across grades and age groups in my own organization. None of it is guesswork. Some of it is regulatory fact, some of it is what I see every filing season, and all of it is the version PSU employees don’t usually get told.

I am not a SEBI-registered advisor or a CA, and views expressed are personal.

The CIBIL Trap: How Over-Leveraging Quietly Ends a PSU Employee’s Loan Eligibility

There’s a pattern I’ve watched repeat itself across grades and age groups in my organization. It usually starts small: a personal loan for a wedding, a bike, home renovation. The EMI fits comfortably against the salary, so a second loan follows, then a third.

Taking on debt becomes second nature after a point. Each new loan feels manageable on its own, so nobody stops to check what the combined EMI load looks like against take-home pay. Banks do stop to check this, and that’s where the trouble starts.

Lenders typically want your total EMI obligations, including the new loan, to stay within a set share of your monthly income. Once a PSU employee has stacked enough loans, there’s simply no room left on paper for a bank to approve anything more, regardless of how stable the job is. A government salary doesn’t override that math.

The specific number behind this check has a name: FOIR, or Fixed Obligation to Income Ratio. It measures what share of your monthly income is already committed to existing EMIs, credit card dues, and other fixed payments, before a new loan is even considered. Most lenders in India work with a FOIR band of roughly 40 to 55 percent for personal loans, meaning your total EMI outflow, old and new combined, should stay under that mark.

This is not a soft guideline that a good relationship with the branch manager can talk around. If your FOIR crosses the threshold a lender has set internally, the application gets rejected before anyone even looks at the words “government salary” on your slip.

Add a missed payment or two along the way (easy to happen when multiple EMIs are running at once) and the CIBIL score takes a hit. From there, even a well-qualified applicant starts getting rejected by name-brand banks and is pushed toward NBFCs willing to lend at a cost.

NBFCs and the Hidden Cost Behind “Low EMI” Advertising

Once a bank turns down a loan application, the next call is usually to an NBFC. Their advertising is built around one number: a low EMI. For someone already stretched thin, that number looks like relief.

What rarely gets advertised is everything sitting behind the headline EMI: processing fees, documentation charges, and penal charges if a payment slips even by a day. A loan that looked cheaper on the surface can end up costing the borrower more over its full term than a straightforward bank loan would have.

This isn’t a case of every NBFC acting in bad faith. It’s that the full cost structure often only becomes visible after the loan is signed, not before. For a PSU employee who already has limited room in the monthly budget, an unexpected charge shows up at exactly the wrong time.

The next section covers what regulation actually says about this, and where it still falls short of protecting the borrower.

What RBI’s 2024 Penal Charges Rule Actually Changed (and Why It Still Doesn’t Save Borrowers)

In August 2023, the RBI issued a directive on penal charges that took effect from April 1, 2024. Lenders can no longer charge “penal interest,” compounded on top of the loan’s regular interest rate. They can only levy a flat “penal charge” on the overdue amount, and it has to be reasonable and non-discriminatory.

Two details matter here. First, penal charges cannot themselves attract further interest, which was a common trick that let a small missed payment snowball. Second, RBI also introduced the Key Facts Statement requirement around the same period, meant to force lenders to disclose all charges upfront in a standard format instead of burying them in fine print.

On paper, this closes a lot of the gap this article has been describing. In practice, disclosure isn’t the same as comprehension. Many borrowers, including PSU employees under salary pressure and time pressure at a bank branch, still sign without reading the Key Facts Statement line by line.

The rule protects people who read it. It does very little for people who don’t, and NBFCs know exactly which group they’re usually dealing with.

For anyone wanting to check the actual regulatory language rather than take a summary at face value, RBI’s circular on fair lending practices and penal charges is public and worth reading directly.

The Salary Account Merry-Go-Round: Why Your Bank Now Demands an NOC

There’s a quieter part of this cycle that plays out inside the accounts department, not at a bank counter. Once an employee has taken on more loans than their salary can comfortably support, EMIs start eating into every other deduction the salary account can carry.

At some point, there’s no scope left. The obvious next move, at least in the borrower’s mind, is to shift the salary account to a different bank altogether, one where the existing EMI mandates don’t automatically pull from the new account. If the switch goes through, the old lender loses its direct hook into the salary.

This is exactly why my organization, like many others now, only processes a salary account change request if the employee produces a No Objection Certificate from their current lending bank. It’s a direct response to employees trying to outrun their own EMI load by changing where their salary lands. Without that NOC, the request simply doesn’t move forward.

This policy exists precisely because of the pattern feeding personal loan rejection for PSU employees down the line. An employee hops banks to escape one EMI mandate, then takes on a fresh loan with the new bank, which pushes their FOIR even higher for the next application. The NOC rule doesn’t fix the underlying debt load, but it does stop the bank-hopping shortcut that used to make the problem invisible to any single lender.

For the lender left without automatic deduction access, the account switch doesn’t erase the debt. It just changes how they collect it, which is where the next part of this cycle takes over.

The Vicious Cycle: Recovery Agents, Blacklisting, and No Way Out

When a salary account switch succeeds, the old lender doesn’t simply write off the loan. They shift to recovery through other means, most commonly a recovery agent contacting the borrower directly, sometimes contacting references listed on the loan application.

This is where the cycle stops being a paperwork problem and becomes a daily-life problem. I’ve written before about what happens on the payroll side when a PSU employee’s loans eat the whole salary, and the pattern described there matches what I see repeat here: employees still paying EMIs on multiple old loans, with little to nothing left from the salary for household expenses once every deduction clears.

Nobody outside the household sees this part. From the outside, the person still has a stable government job and a fixed monthly salary, which looks like financial security. From the inside, they’re often quietly managing a shortfall every single month, covering it however they can.

It’s worth knowing that RBI does place limits on how recovery agents can behave, even though few borrowers use these protections. Agents can only contact borrowers within specified daytime hours, cannot use threatening language, cannot contact a borrower’s employer or family without consent, and must carry identification when visiting in person. Any PSU employee dealing with aggressive recovery calls has the right to escalate the matter to the bank’s grievance officer and, if unresolved, to the RBI Ombudsman at no cost.

This is the actual cost of the loan-stacking pattern behind most cases of personal loan rejection for PSU employees: not just rejection at the next bank counter, but a standard of living that keeps shrinking long after the loans were taken.

How to Avoid Personal Loan Rejection as a PSU Employee: Practical Steps

The good news is that most of what causes personal loan rejection for PSU employees is preventable with a few disciplined habits, not luck or connections at a bank.

Start by checking your CIBIL score before you ever apply, not after a rejection. Most banks and several free apps let you pull this once a year at no cost, and it tells you exactly where a lender will see risk before you find out the hard way.

Keep your total EMI outflow, across every loan and credit card, well under half your take-home salary. This is the single habit that would have prevented most of the cases described earlier in this article. If you’re already near that limit, the answer is to close a loan, not open a new one.

You can calculate your own FOIR before applying, the same way a bank will. Add up every existing EMI and fixed monthly obligation, divide by your net monthly income, and multiply by 100. If the number comes out above 50 percent, expect resistance from any lender, and treat that as your signal to pay down existing debt before submitting a fresh application.

Before signing anything with an NBFC, read the Key Facts Statement RBI now requires them to provide. It’s short by design specifically so it gets read, and it will show the real cost of the loan rather than just the advertised EMI.

Finally, if you do plan to switch your salary account for any reason, get ahead of the NOC requirement early. Approach your current lending bank before your accounts department asks for it, since waiting until you need the switch urgently only adds delay and stress you don’t need.

Treat these four steps as prevention, not damage control after personal loan rejection for PSU employees has already happened. Every one of them is something you control directly, unlike the lending decision itself, which sits entirely with the bank.

Bottom Line

Personal loan rejection for PSU employees isn’t really about the job or the salary. It’s about what happens to that salary once too many EMIs are already pulling from it, and how little room some lenders leave for anyone to see that coming.

None of the patterns in this article are unique to any one bank, NBFC, or organization. They repeat across grades, ages, and departments, which is exactly why they’re worth naming plainly instead of treating each case as a personal failure.

If there’s one habit that changes the outcome, it’s checking your total EMI load against your salary before a bank does it for you, and reading the Key Facts Statement before signing anything that promises a low EMI.